If you need assistance with currency trading to meet the shorter security settlement, or if you have derivatives trading requirements, Mesirow Currency can help. Please call Joseph Hoffman at 312.595.2019.

In May 2024, the US, Mexican and Canadian securities markets moved from a settlement period, or cycle, of two days after trading (T+2) to one day (T+1). That means investors (the securities owner or securities manager) began exchanging securities and cash one business day after trading. These North American nations joined India and China in the vanguard of countries settling sooner than T+2. Other nations and regional markets are likely to move to T+1 to align with North American trading; some nations are even evaluating a T+0 settlement cycle, exchanging securities and cash in almost real-time.

Reducing the settlement cycle by half affects the time allotted to security processing which, in turn, affects currency trading for foreign investors. Those investors need local currency – US dollars, Canadian dollars, and Mexican pesos – to purchase North American securities.

Many foreign exchange (FX) transactions settle T+2. In a currency settlement, the participants in the transaction receive the currency they bought and deliver the currency they sold. The two-day settlement cycle has existed since the 1980s – and likely earlier – as the conventional FX settlement cycle.

This change in the securities settlement cycle also affects the conventional foreign exchange settlement process.

An Australian investor would need to convert Australian dollars to US dollars to buy equities on a US exchange. Given time zone differences that cause Australia to be one day ahead of North American markets, Australian investors are settling the transaction the same day as the North American securities execution.

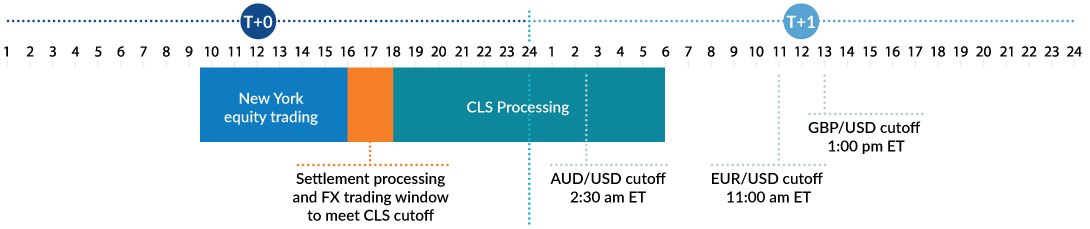

Often, a currency order is issued after security processes such as allocation and confirmation are completed, compressing the time available to get the currency trade done. And the shorter currency settlement cycle also affects CLS, the industry settlement service, which has a deadline two hours after equity trading finishes. Although short settlement cycle deals can be completed on time, the process often requires human assistance, slowing the process and increasing the likelihood that something will go wrong.

The conventional currency settlement cycle is also affected by regulatory pressure and technological advances. Regulators are urging the FX market to move to T+1 settlement too. In January 2024, Gary Gensler, the chair of the US Securities and Exchange Commission, spoke to a European roundtable conference about the securities industry's move to a T+1 settlement cycle. The US SEC chair said that the currency settlement cycle should also be decreased to T+1: "time is money, time is risk..."

Technology is pushing FX payments into the next generation. Rapid payment systems like India's Unified Payments Interface, China's payment apps, Alipay and WeChat, and its payment messaging system (CIPS) are focused domestically. But the enormous popularity of these two nations' payment systems has India and China aiming for international customers.

India and Singapore have connected their systems so that consumers can use familiar apps to pay in the other nation with FX transactions occurring behind the scenes. India is talking with over 20 other nations to link systems, and China has tested cross-border systems using central bank digital currencies, an electronic form of a nation's currency. These systems typically support person-to-person or business-to-consumer transactions, but institutional investor cross-border payments would be a natural extension.

Outsourcing currency trading and settlement is an alternative to in-house management. Some investors are considering using the custodian of the securities account to manage the currency transactions. But this solution could undo the tremendous effort that investors have expended over the last two decades to meet their fiduciary duty to get the best price in a currency trade. Custodians typically do not have a fiduciary obligation to manage foreign exchange transactions, a troubling shortcoming for investors who have a fiduciary duty to their clients.

Outsourcing foreign exchange transactions to a specialist manager who is a fiduciary can be a pragmatic choice. Besides meeting the investor's fiduciary responsibilities, outsourcing foreign exchange transactions to a specialist can mean a better allocation of scarce resources.

Investors select securities managers because of the managers' expertise with securities, not foreign exchange trading. Given that client emphasis on securities, it would be reasonable for the manager to assign the firm's best staff and spend money and time on securities trading and settlement, not foreign exchange. The result is potentially poor FX outcomes, more risk and less efficiency in post-trade processing. An FX manager, on the other hand, can likely provide superior execution at less risk and cost than the securities manager.

Shorter settlement cycles are another reason to use a foreign exchange expert. Currency settlement is increasingly complex, and a currency manager with sole focus on foreign exchange trading and settlement has the expertise and technology to get the best price and settle the transaction on time and without incident.

A securities manager might balk at the inclusion of another party in the trading and settlement process, claiming that the new party increases operational risk and process complexity. But third-party foreign exchange trading is a common arrangement in the securities industry, and most currency managers have years – even decades – of experience seamlessly integrating processes with securities managers.

Investors must wonder at the cost of these upcoming transformations – does it make sense to spend enormous resources adjusting to rapid change in currency settlements and payment processes? How does this effort fit with the investor's financial mission to improve investment performance? And if the investor thinks the cost exceeds the benefit, what should the investor do?

The securities manager can view the currency specialist as a partner in the investment process. The securities manager has expertise in securities management and the currency specialist brings equal proficiency in foreign exchange matters. Combined, the two specialists offer complementary investment competence, providing their client with a superior investment capability.

Those complementary skills can help meet a challenging operational situation. One hour between the close of the North American securities market at 4 pm Eastern Time and the end of the currency trading day at 5 pm leaves little time for handling exceptions and solving problems. Two managers – one with expertise in securities and the other in currencies – can jointly address problems, match trades and complete the currency process.

The hour window also involves concerns about reduced currency trading volumes as regional trading switches from North America to Asia. When demand is high those lower volumes can mean increased trading costs. A currency specialist can overcome this low-liquidity period by matching unrelated orders to benefit all clients involved in the match. Euro buy orders from security-settlement clients can be matched with euro sell orders from return-seeking clients thereby reducing the amount of trading required during this thin period of liquidity.

The currency manager might also be able to help clients with other services such as currency hedging, currency investing for return and derivatives trading in other instruments to improve investment performance.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.