Insights

Get It Wholesale

Share this article

May 30, 2023 | By Mesirow Currency Management

Foreign exchange trades settle two days after trading. Could they settle in 30 seconds?

Foreign exchange settlement risk, the risk that one party to a currency transaction won’t receive the currency it purchased, is increasing. While most currency deals conclude without incident, the growing volume of transactions that could fail has regulators searching for better ways to settle foreign exchange trades. In this article, we describe the size of the foreign exchange market, the currency deals that are vulnerable to settlement risk, and the ways that currency traders manage settlement risk—or why they don’t.

We’ll also examine possible improvements to the settlement process, particularly a more widespread adoption of payment versus payment systems in FX settlements and also look at the promising potential of central bank digital currencies.

Foreign exchange settlement risk on worrisome upswing

$2.2 trillion at risk of failure each day

A foreign exchange (FX) transaction consists of two parts: trading and settlement. Trading determines the details of the transaction: the exchange rate (the trade’s price), the currencies and amounts to be exchanged, and the date of that exchange, or the settlement date. The second part of an FX transaction, settlement, involves the steps to exchange the currencies and amounts traded. A behind-the-scenes process, settlement is only noticed when a large settlement fails. Because settlement failure can be catastrophic, regulators are searching for ways to reduce settlement risk, the risk that one party to an FX transaction will not deliver the currency it sold.

Ways to cope with settlement risk

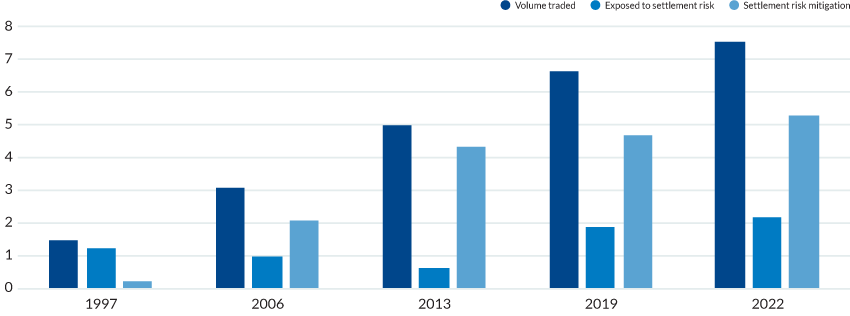

The foreign exchange market is huge: The Bank for International Settlements research reported an average of $7.5 trillion was traded each day in April 2022. While foreign exchange trading volumes have increased five-fold since 1997 (Figure 1), the volume of transactions that are exposed to settlement risk has increased only 74 percent. Still, the tremendous growth in foreign exchange trading volume has resulted in an average of $2.2 trillion of transactions vulnerable to settlement risk each day.

Figure 1: Average Daily Foreign Exchange Trading Volume and Transactions Exposed To Settlement Risk - $ Trillion Per Day

Sources: Bank for International Settlements, FX settlement risk: an unsettled issue https://www.bis.org/publ/qtrpdf/r_qt2212i.htm | Kos, D and R Levich, "Settlement risk in the global FX market: how much remains? - CLS Insights, 26 October 2016

Most failed settlements are small and unrelated. But even small failures can be costly and painful, consuming significant resources to determine the cause. There could be considerable correspondence between parties regarding blame and compensation, as well as overdraft and interest costs. More unsettling, a series of large failures involving one or more systemically important financial institutions could spread to other sectors, resulting in substantial risk to the global economy.

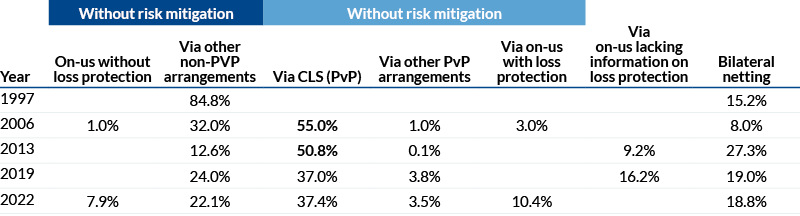

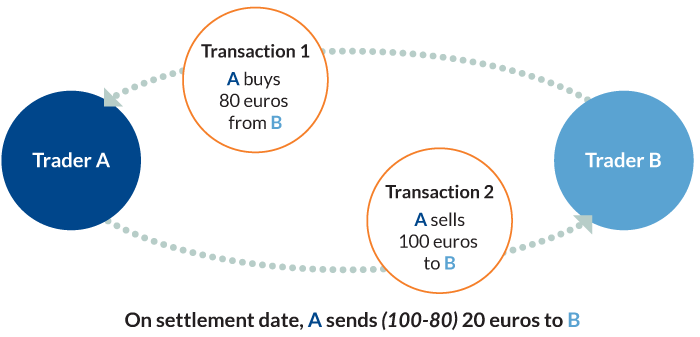

Market participants have a few ways to manage settlement risk. Bilateral netting, a long-standing and popular risk management method, was used in a little less than one-fifth of all transactions in 2022 (Table 1). Trades in the same currencies for the same settlement date are netted and only the difference is transferred. Figure 2 presents a simple case of bilateral netting.

Table 1: Foreign Exchange Settlement1 Methods

1. Settlement as a percentage of deliverable turnover. | Source: Bank for International Settlements, FX settlement risk: an unsettled issue https://www.bis.org/publ/qtrpdf/r_qt2212i.htm

Figure 2: Bilateral Netting Example

Source: Mesirow Currency Management

Bilateral netting was the principal way entities managed settlement risk before the development of Continuous Linked Settlement, the international payment system for settling foreign exchange transactions. Launched in 2002, CLS is a payment versus payment (PvP) system, meaning a transaction is settled only if CLS has received both payments from the two trading parties. If one party fails to deliver its currency, CLS returns the other party’s payment.

CLS is a multi-lateral settlement system for eighteen of the most traded currencies; most are currencies of advanced economies such as the US, Europe, and Australia. CLS is not available for most emerging market economy currencies. However, trading in the Malaysian ringgit, the Chinese renminbi, and the Indonesian rupiah, among other emerging market economy currencies, are booming, reaching 22.6 % of global turnover in 2019 and almost 25% in 2022, and the ineligibility for CLS settlement is reflected in the drop in CLS settlement rates for 2019 and 2022 (Table 1).

On-us settlement is another, though less popular, risk mitigation means. On-us settlement means the two parts of a trade are settled at a single entity. For example, a client instructs its bank to buy euros by selling yen. Settlement risk exists, however, unless the euro portion and the yen portion of the trade are booked simultaneously. Often the bank is dealing with subsidiaries or branches located in different time zones, preventing simultaneous settlement and giving rise to settlement risk. On-us risk can be mitigated with pre-authorized credit lines.

Why don’t more traders manage settlement risk?

Several reasons explain why the volume of transactions exposed to settlement risk have increased.

Some currency market participants take advantage of automated bilateral netting, but for others in emerging market economies (EME), bilateral netting can be manual, a tedious and time-consuming process. Most EME currencies aren’t eligible for CLS settlement, and other PvP methods might not be available either. For example, Hong Kong’s CHATS system offers PvP settlement for the US dollar and Chinese renminbi (the most traded currency pair involving an EME currency), but access to CHATS is limited to Hong Kong SAR and banks in Indonesia, Malaysia and Thailand.

Even if CLS and other PvP settlement methods are available, users may conclude that the settlement benefits aren’t worth the technical cost to connect to the PvP system, the effort to modify existing operations, or the expense of transaction charges and monthly fees. Other considerations may influence the decision not to participate in PvP settlement. These may include a view that settlement risk is not enough incentive to use a PvP system.

Finally, time zone differences and the strict deadlines for submitting transactions to the PvP system may conflict with liquidity requirements resulting in the decision to forgo PvP settlement in favor of better liquidity opportunities.

Potential settlement risk enhancements

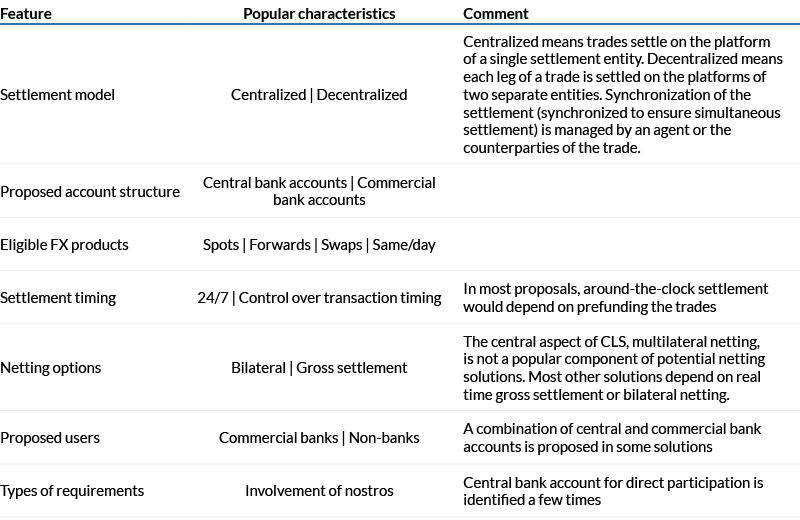

In October 2021, the Committee on Payments and Market Infrastructure asked commercial banks, fintech companies and other interested parties to share ideas for promoting increased adoption of PvP. Table 2 summarizes some of the most popular ideas for improving PvP usage.

Table 2: Proposed features for increasing the adoption of PvP in FX settlements

Source: Committee on Payments and Market Infrastructures, 2022. https://www.bis.org/publ/qtrpdf/r_qt2212i.htm

Project Cedar and the future of foreign exchange settlements

Central bank digital currencies (CBDCs) are a digital form of government-issued currency held in an account at the nations’ central bank. Eleven nations have issued CBDCs for retail and commercial use, and eighteen nations are in pilot phase. The nations that have launched CBDCs are encountering a rocky start. Designed for retail users, CBDCs have experienced problems including poor marketing, unfamiliarity with the new currency form, a paucity of merchants willing to accept the digital payments, and worries about privacy.

Wholesale central bank digital currencies (wCBDC), in contrast, are limited to commercial banks and financial firms and have a promising potential to make foreign exchange settlements almost instantaneous, to minimize counterparty risk (the risk that a party to an FX trade might default on its obligations), and to reduce the number of intermediaries involved in settling a foreign exchange transaction.

Project Cedar, overseen by the Federal Reserve Bank of New York, was a test of a simple foreign exchange transaction using wCBDCs and distributed ledger technology, a digital system for recording the transaction of assets in which the transactions and their details are recorded in multiple places at the same time. The test was successful and demonstrated that foreign exchange transactions could:

- Be settled in less than 30 seconds, a vast improvement over the current-day settlement standard of two days

- Reduce settlement risk by simultaneously settling both currencies

- Result in transactions that are more transparent, convenient (by enabling payments 24/7/365), and flexible (by involving distributed ledgers of a wide variety of financial institutions)

Project Cedar’s Phase 1 Report was published last fall, and Phase II which aims to “enhance designs for atomic settlement of cross-border cross-currency transactions, leveraging wCBDCs as a settlement asset” was announced in November 2022.

Wholesale CBDCs, which are limited to commercial banks and financial firms for currency deals, might be a better way to promote central bank digital currencies compared to CBDCs designed for retail users.

A wholesale application of CBDCs would have a well-defined problem to solve (increase FX settlement rates), high incentive to address a potentially devastating situation (systemic risk from a large-scale currency settlement failure), technically savvy users, and fewer worries about the protection of personal privacy. Wholesale central bank digital currencies for foreign exchange settlements could be the perfect application of the new digital currency.

Explore

Central Bank Digital Currencies

What do CBDCs mean for the US dollar as the world’s major reserve currency?

Read article

US dollar: Currency dynasty

Is the USD's position as the world's reserve currency safe, or is its decline inevitable?

Read article

Spark

Our quarterly email featuring insights on markets, sectors and investing in what matters