Postwar gold standard: "As necessary... as a police force and tax collector" Montagu Norman, Governor of the Bank of England1

The death, destruction and devastation that followed the Great War (1914 – 1918) could not have been more apocalyptic. Eight million dead, fifteen million wounded, a third of the German male population between 19 and 22 years wiped out. Northern France, the host of horrific battles, was a post-war scene of indescribable wastage. No wonder the ordinary person longed for the peace and prosperity of the Victorian and Edwardian era that preceded the conflict.

A major part of that era, in many minds (not the least in the minds of those in position to advocate for economic policy), was the gold standard. The longing ignored Benjamin Disraeli's view that a nation's gold reserve was a result of that pre-war period and not the cause of the good times. The question was how to get back onto a gold standard from a wartime economy.

For Great Britain, the world's financial leader and gold standard bearer, the obstacles were formidable. The price level after the war was three times that of the pre-war period (the price level was important because more gold was needed to match pre-war purchasing power); the price-level in 1925 was still twice the pre-war level. Debt was crushing, and British industry was uncompetitive.

Exports were down 25 percent compared to before the war, but the demand for imports was strong. Because imports exceeded exports, Great Britain needed to borrow to fund the difference. That borrowing pressured the gold stock when lenders insisted on repayment in gold instead of paper currency.

To reverse capital flows, the Bank of England resorted to increased interest rates that throttled business and reduced employment. High unemployment meant lower wages, steady (or falling prices) which, combined, strengthened the exchange rate in Great Britain's favor. The downside to higher interest rates was widespread misery for labor, which saw one million laid off after the Bank of England hiked interest rates in 1920.

More labor agony was to follow. After passage of the British Gold Standard Act of 1925, many cheered, but not the seven million workers unemployed since the start of the year. Their numbers would mount rapidly as Great Britain and most of the world drew closer to the Great Depression. And when capital flowed from Europe to the US to participate in the astounding stock market, those nations tried to arrest gold outflows with their own brand of economic austerity.

These nations' participation in the US stock market was too late; when the market crashed in October 1929, Britain, Germany, Austria and Italy were already on their way to depression.

It is inconceivable to us in the 21st century that economists, central bankers and treasury officials in the 1920s and 1930s did not recognize that the dire economic situation demanded liquidity and increased government spending. But few – most vocally the British economist John Maynard Keynes – did.

Instead, the loudest voices demanded nations maintain gold levels and stay on the gold standard. President Hoover thought that gold was essential to protect people's savings from inflation and deflation. In early 1933, when the depression intensified, a large band of economists demanded that the US rigidly maintain the current gold standard. Doing anything else would diminish confidence and slow recovery, they claimed.

Senator Carter Glass declined Franklin Roosevelt's invitation to become Secretary of the Treasury because Roosevelt would not guarantee that the United States would remain on the gold standard. Journalists, Congressional leaders and George Harrison, the chief executive officer of the Federal Reserve Bank of New York, forcefully agreed.

So instead of flooding their nations with the one asset that everyone wanted – cash - nations reacted to the unfolding horror by draining liquidity from the financial system. Officials increased interest rates, refused to provide social safety nets, raised import duties and balanced budgets by hiking taxes. The gold advocates had one objective: maintain the nation's level of gold no matter what. 'No matter what' meant incomprehensible financial and personal disaster for many people around the world as shown in Table 1.

Conditions were so bad, that no matter how hard officials tried – and they tried extraordinarily hard, heaping taxes upon cuts in spending upon higher interest rates - maintaining gold levels was impossible.

One by one, countries fell off the standard. The collapse of Austria's largest bank, Creditanstalt Bank in May 1931, ignited banking panics and collapses in surrounding countries, including Germany. To respond to a declining reichsmark and outflow of gold, Germany enacted such complex currency controls that the nation effectively ended its gold standard in 1932.

Great Britain gave up in late 1931 when the Bank of England asked the government to end its obligation to provide gold bullion on demand. Other nations quickly followed Great Britain's actions so that in a year's time only 24 of 47 countries remained on the gold standard. Six years later, no one remained.

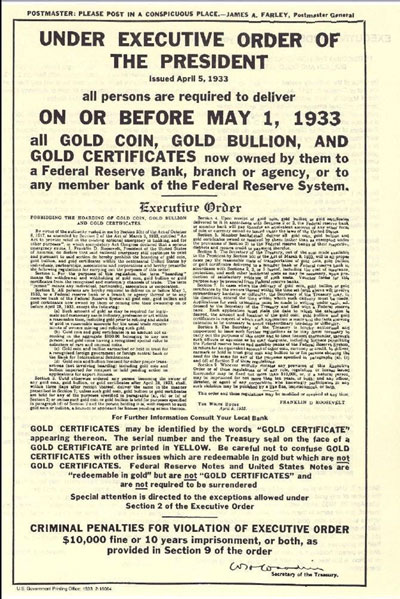

Urged by President Hoover to follow a deflationary strategy in a misguided attempt to revive the economy, Congress complied. But with the economy collapsing, newly elected President Roosevelt's Emergency Banking Act of 1933 allowed the President to prohibit the export or hoarding of gold, and it gave the Treasury power to demand the surrender of gold and gold-like currency, effectively ending the US participation in the gold standard.

Things gradually improved and then worsened again until January 1934 when the United States changed the value of an ounce of gold from $20.37 (set in 1837) to $35, a price that would last until 1971. Changing the price of gold was not the only catalyst for improving economic conditions, but from 1933 to 1937 unemployment declined from 25 percent to 14 percent and industrial production increased 60 percent.

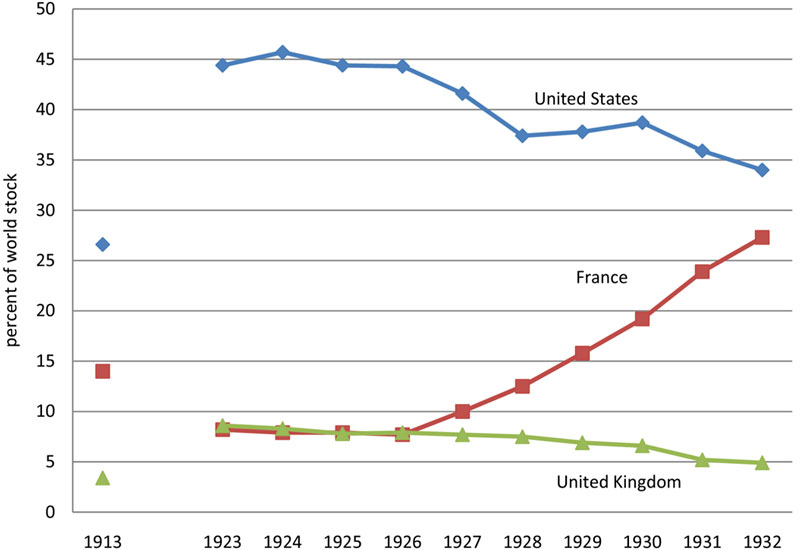

France took longer than most countries to remove itself from the gold standard. As banking and credit turmoil moved from country to country, gold flowed from those nations to others perceived to be safer, such as France. But the French couldn't outrun the financial catastrophe. After the British uncoupled the pound from gold in 1931, the franc looked expensive.

Deflation caused prices to decline about 25 percent between 1931 and 1935; in the same period, French national income fell by a third. Things increasingly worsened so that the nation was devastated by sit-down strikes that, among other things, led to an end of the gold standard and devaluation of the franc in September 1936.

As nations left the standard their currencies devalued, causing the price of gold to rise. The rise in the precious metal's price caused production to soar. That increased mining coupled with gold from Asia made its way to western central banks. The Federal Reserve was the end recipient of this gold because the Fed was willing to buy everything that glittered at $35 per ounce. By the start of World War II, 60 percent of the world's gold was stored in the US.

Besides getting a good price for gold, storing it in America was viewed as protection against alarming events in the world, not only the economic catastrophe of the Great Depression, but political situations such as the rise of National Socialism in Germany, fascism in Italy, and the territorial aims of Japan.

Our third article on gold as money. Gold botched the recovery of post-WWI economies and worsened the Great Depression. Did it have better luck reviving the global economy after WWII?

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.