When planning how to donate to charitable causes, it is important to be aware of all of the tax implications. Two strategies often used by individuals and families are donor-advised funds (DAFs) and private foundations; each has unique costs and tax advantages.

DAFs allow you to gift cash, appreciated securities, or other assets directly into a fund, then help choose which charitable organizations the fund makes grants to. DAFs are relatively easy to set up and inexpensive to maintain. You have the ability to make donations from the fund and are not subject to minimum annual donations. DAFs are also characterized with low startup costs, tax deductions and minimal time commitments.

DAFs have notable tax advantages. Under current law, an individual’s adjusted gross income (AGI) can generally be reduced by up to 60% for cash donations or 30% for long-term appreciated assets contributed to qualifying public charities, compared to 30% and 20%, respectively, for most private foundations.1,2,3 Beginning in 2026, new federal rules also apply a 0.5% AGI “floor” before itemized charitable deductions are allowed and introduce a modest universal charitable deduction for some non-itemizers; these changes do not alter the percentage limits above but may affect how much of a given year’s giving produces a current-year tax deduction. This can be incredibly useful in years with a large tax bill, as you can donate a large sum to a DAF and then recommend grants to charities over several years.

One key limitation of DAFs is that the donation must be made to a 501(c)(3) public charity such as Make-Wish America, religious organizations, or educational institutions. DAFs cannot donate to individual causes or charities that are not characterized as a 501(c)(3)5. More about DAFs.

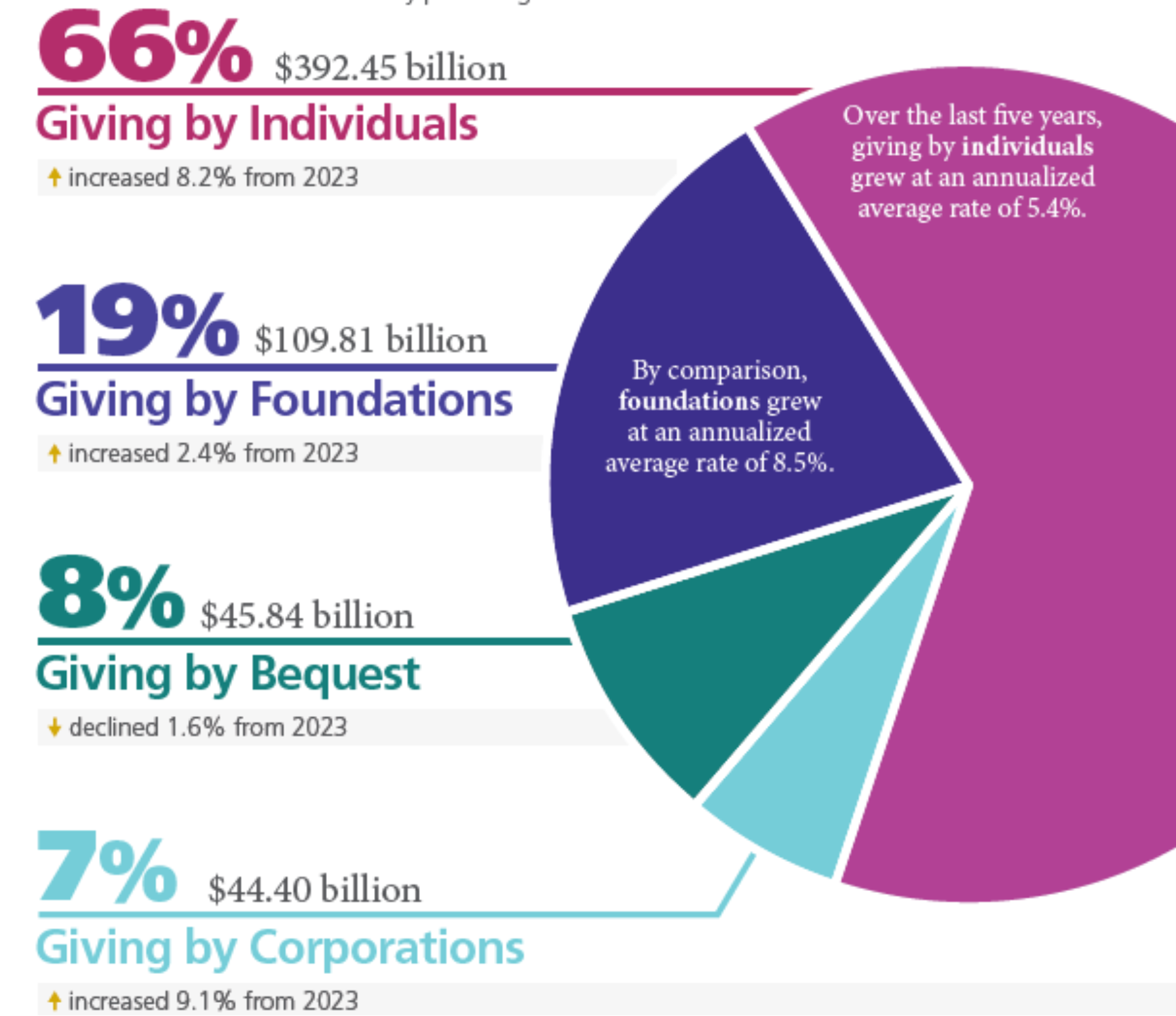

As seen in the chart below, based on Giving USA 2025 (reporting on 2024 data), foundations made up approximately 19% of charitable giving in 2025 and grew about 2.4% from 2023. Private foundations continue to be a meaningful and growing source of charitable giving and can be a tax-advantaged vehicle for you to support the causes that mean the most to you and your family.

Private foundations have several pros and cons compared to a DAF. Foundations are often associated with a ‘prestige’ element where wealthy individuals create a fund with a specific goal of donating to charitable causes that mean the most to them. Foundations can make grants with fewer restrictions compared to a DAF to help ensure that donations are aligned with the donor. A private foundation is designed to last in perpetuity with a requirement to donate 5% of net assets annually.3

However, foundations can be incredibly expensive to organize and operate. You should consider hiring legal and accounting professionals to handle startup and ongoing regulatory and compliance matters like bookkeeping, tax preparation and corporate filings. If the net assets of the foundation are not high enough, these expenses can quickly deteriorate the corpus of the fund and make the foundation unfeasible.

While both strategies allow up to grow your donations with minimal taxes, there are several differences to consider. In order to determine which strategy is best for you, it is important to be aware of the key differences between DAFs and private foundations:

Sources: Mesirow, IRS, NCFP, Moss Adams, Giving USA

When considering if setting up a private foundation or a donor-advised fund is consistent with your charitable goals, it is important to consider the pros and cons to both strategies and alternative options, such as giving directly to a charity that is aligned with your values. Please discuss each of these charitable strategies with your wealth advisor and other professional resources before making any material donations.

Mesirow does not provide legal or tax advice. Past performance is not indicative of future results. The views expressed above are as of the date given, may change as market or other conditions change, and may differ from views express by other Mesirow associates. This is not a solicitation to buy or sell the securities mentioned. Do not use this information as the sole basis for investment decisions, it is not intended as advice designed to meet the particular needs of an individual investor. Information herein has been obtained from sources which Mesirow believes to be reliable, we do not guarantee its accuracy and such information may be incomplete and/or condensed. All opinions and estimates included herein are subject to change without notice. This communication may contain privileged and/or confidential information. It is intended solely for the use of the addressee. If you are not the intended recipient, you are strictly prohibited from disclosing, copying, distributing or using any of the information. If you receive this communication in error, please contact the sender immediately and destroy the material in its entirety, whether electronic or hard copy. This material is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.

Mesirow Wealth Management is a division of Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor. Securities offered through Mesirow Financial, Inc., member FINRA, SIPC. Advisory Fees are described in Mesirow Financial Investment Management Inc.’s Part 2A of the Form ADV. Mesirow refers to Mesirow Financial Holdings, Inc. and its divisions, subsidiaries and affiliates. The Mesirow name and logo are registered service marks of Mesirow Financial Holdings, Inc.