Financial terminology can sometimes seem like a different language. Financial news reports can seem daunting to try to understand what is being said and how it impacts a person's everyday life.

To make things simple, here are five essential finance terms we believe everyone should know:

Through this high-level overview, we hope to provide helpful information to make everyone feel more confident about their financial knowledge.

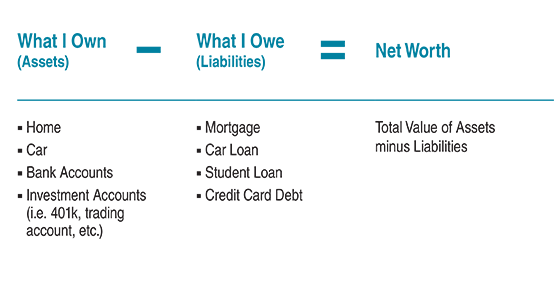

Simply put, net worth is the value of everything that you own (also known as your "assets") after accounting for everything that you owe (referred to as "liabilities").

Knowing your net worth is important because it gives you an idea of your overall financial health. You want to have a positive net worth when possible. It can also help you understand your various types of obligations on your loans. Certain loans, such as mortgages, often have lower interest rates (fees for borrowing the money) than credit cards. When deciding what loan to pay off first, it can be helpful to prioritize paying off the loans with the highest interest rate. Understanding your loans might also help you see if there is an opportunity to refinance or get a lower rate of interest by working with your lender.

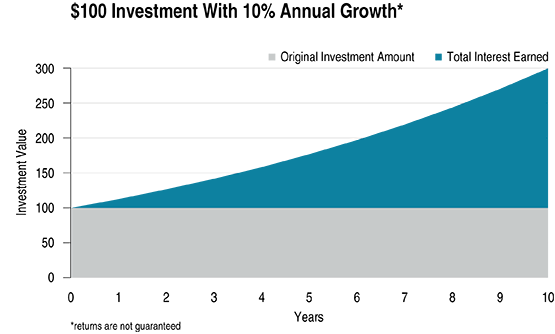

Also referred to by Albert Einstein as the "eighth wonder of the world," compounding can be thought of as growth on your growth. When referring to savings or investments, compounding is what happens when instead of taking out the money that is earned on your investment, you let it stay invested and earn interest on your interest.

Compound interest can also refer to loans, meaning the longer it takes you to pay off your loan, the more you end up paying in interest. This is why Albert Einstein's quote finishes,"He who understands it, earns it - he who doesn't, pays it."

* The chart above contains hypothetical returns of 10% for illustrative purposes only.

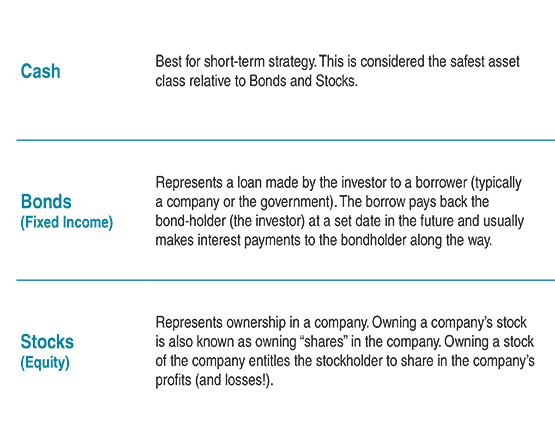

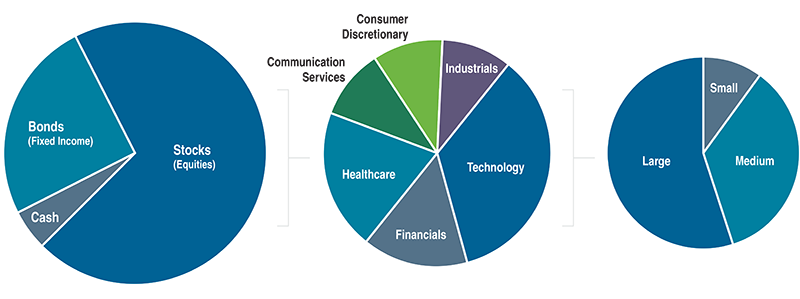

Asset allocation is how your money is invested into different categories known as asset classes. Broadly speaking, the main asset classes include cash, bonds (also knowing as "fixed income"), stocks (also known as equities). Your asset allocation is determined by the amount of money you have invested into each of these asset classes.

Each of these asset classes carries its own set of risk and return profiles. Typically, a stock has more growth potential than a bond, but it also has more volatility. Volatility can lead to a wide range of outcomes, some of which involves loss. Keep in mind that volatility itself is not risk. Risk, rather, is the possibility of permanent loss. Beware though, there are some cases where certain bonds might have more risk than a stock.

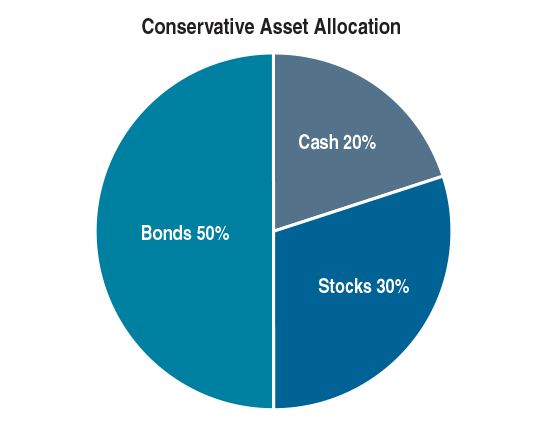

* Source: Mesirow. Past performance is not necessarily indicative of future results,

Deciding which asset allocation is best depends on an investor's goals, risk tolerance, and time horizon. The chart on the right would be considered one potential version of a conservative asset allocation. Someone who is investing for long-term growth, such as a recent college graduate who is saving for retirement, would invest more heavily in stocks. Understanding your goals, time horizon, and risk tolerance are all key factors in determining your asset allocation.

Imagine you had $1 million dollars to invest and you were 100% confident that investing in a single individual stock would grow to $10 million after 10 years. That would be great, right? Well unfortunately, individual stocks have a wide range of outcomes. If you put your entire $1 million in this stock and it went to $0, you would suffer a massive loss with no money left to start over. This is why diversifying or investing across various asset classes and various investments is the key to a successful portfolio.

Diversifying your investments across different asset classes is important but it is also important to diversify within those asset classes by investing in companies that vary based on their industry, company size, and other factors. By diversifying, you are spreading (and likely reducing) your risk across different types of investments.

Once you begin to invest, the hope is that your investments rise in value. If you choose to sell a position, which may happen to get back to a desired asset allocation, diversify investments, or raise money to make a purchase, you create a "realized gain" or "realized loss." This is the difference between what you paid for an investment and what you receive from its sale. If you have made money through the investment, you are required to pay taxes on the gain, known as a capital gains tax.

Typically, your capital gains tax rate will depend on your income level and how long you have held the investment. An investment that is sold for a gain before one year would create a short-term capital gain. Any investment held for more than a year is considered a long-term capital gain. If you happen to lose money in an investment and sell it for less than what you bought it for, you will have a capital loss. For tax purposes, your capital losses will be subtracted from your capital gains in order to determine your tax bill.

Certain accounts, such as retirement accounts, will not incur a tax from sales until you begin to withdraw money from the account. In a taxable account, however, you will pay taxes on the sales in the year that the investment is sold.

Mesirow Wealth Management works with investors like you to help you develop a financial plan that makes sense for your unique situation, and is committed to ensuring that you understand how your investments are integrated with your plan.

Learning the ins and outs of financial terms isn't always easy, but partnering with an advisor that you trust can be a great first step.

Mesirow does not provide legal or tax advice. Past performance is not indicative of future results. The views expressed above are as of the date given, may change as market or other conditions change, and may differ from views express by other Mesirow associates. This is not a solicitation to buy or sell the securities mentioned. Do not use this information as the sole basis for investment decisions, it is not intended as advice designed to meet the particular needs of an individual investor. Information herein has been obtained from sources which Mesirow believes to be reliable, we do not guarantee its accuracy and such information may be incomplete and/or condensed. All opinions and estimates included herein are subject to change without notice. This communication may contain privileged and/or confidential information. It is intended solely for the use of the addressee. If you are not the intended recipient, you are strictly prohibited from disclosing, copying, distributing or using any of the information. If you receive this communication in error, please contact the sender immediately and destroy the material in its entirety, whether electronic or hard copy. This material is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.

Mesirow Wealth Management is a division of Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor. Securities offered through Mesirow Financial, Inc., member FINRA, SIPC. Advisory Fees are described in Mesirow Financial Investment Management Inc.’s Part 2A of the Form ADV. Mesirow refers to Mesirow Financial Holdings, Inc. and its divisions, subsidiaries and affiliates. The Mesirow name and logo are registered service marks of Mesirow Financial Holdings, Inc.