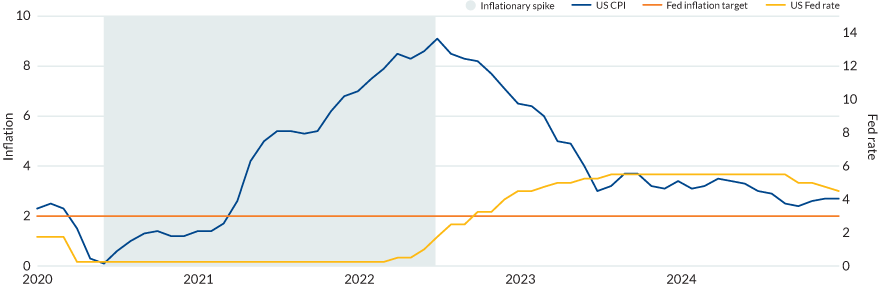

Inflation had been on a productive trajectory lower since peaking in the US in mid-2022. However, the inflation fight was harder to win than expected as lingering CPI led the Fed to pause, keeping rates high-for-longer to combat its stickiness.

This, and the Republican clean sweep in the US election, led to the US dollar outperforming the rest of the G10 currencies in 2024. As Trump begins his second term and geopolitical uncertainty continues this coming year, policy ramifications and global instability will keep investors vigilant in 2025.

With US inflation falling substantially in 2023 towards 3%, the market pivoted its focus away from inflation and more towards the labor markets, assuming that the inflation fight was being won and that the path lower would continue in 2024. However, progress stalled as the path lower became a slow grind (Figure 1), with the most recent inflation print before year-end coming in at 2.7%, above the Fed's long-run target of 2%.

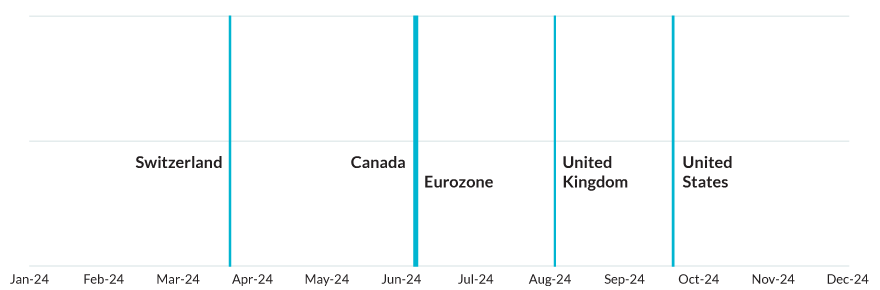

The Fed response was to pause, with a later start to its cutting cycle (September 18, 2024) than most other central banks (Figure 2).

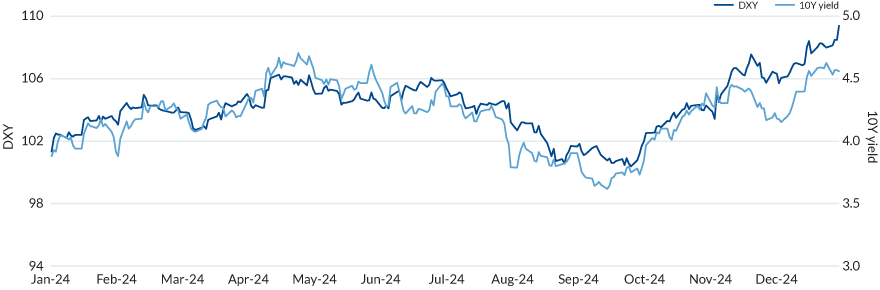

With the Fed following the high-for-longer playbook, the dollar found support over the first half of 2024 before labor concerns came more into focus, capped by the large negative data revision released during the summer. The dollar was under pressure in Q3, with falling yields responding to the cooling labor market.

In the past year, yields acted as a reliable reflection of Fed expectations. 10Y yields tracked the US dollar index consistently throughout the year, moving in sync across both USD-positive and USD-negative periods (Figure 3). Throughout the many news events and cycles in 2024, FX market behavior often distilled down to central bank expectations, with the dollar reacting to the Fed.

Leading into the election in November, a Trump victory was considered dollar-positive based on presumed policy changes and the dollar response to those policies. Tariffs can reduce supply and raise inflation, prompting the Fed to keep rates higher. Corporate tax cuts can support equities, leading to more investment flows into the United States.

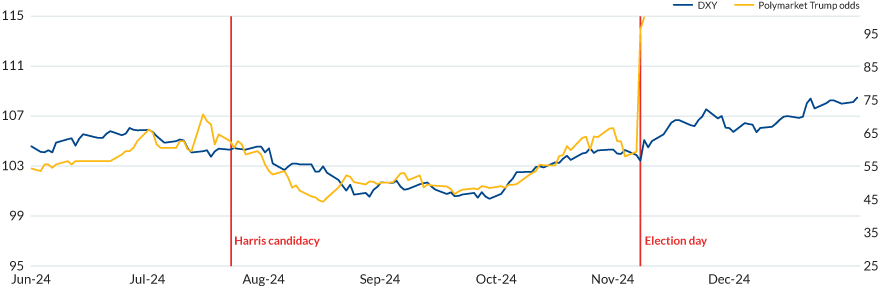

The US election outcome became a popular bet on the prediction markets. As the election approached, the dollar moves were in sync with the odds of a Trump victory. The US dollar index and Trump's odds per Polymarket tracked remarkably well in the months leading up to the election (Figure 4).

When Kamala Harris became the democratic candidate over the summer after Joe Biden exited the race, Trump's odds began to lower, and the dollar followed suit. As Trump's odds improved in the early fall, so did the dollar, appreciating into the election. The Republican clean sweep propelled the dollar even higher, and it rode that wave into year-end.

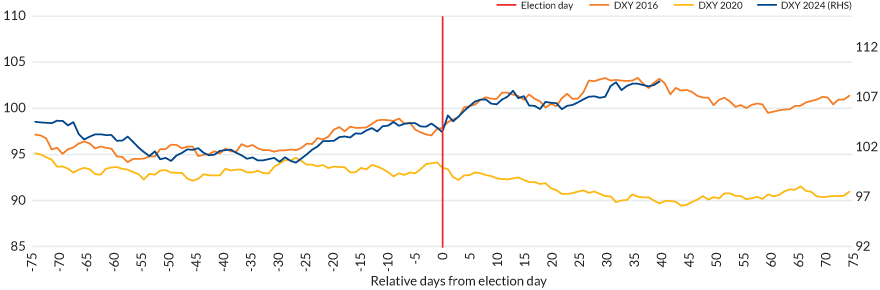

The US dollar path surrounding Trump's 2016 victory has been repeated in the movements surrounding the 2024 election. Charting seventy-five days prior to and then after Election Day for the past three election cycles, 2016 and 2024 are staggeringly similar from before the election through the end of the year (Figure 5).

Following the dollar direction subsequent to the 2016 election would imply an eventual tapering of US dollar strength in the first quarter of 2025. The dollar movements around Biden's 2020 win were dissimilar from the Trump victories, helping to distinguish the difference from a seasonal or election period tendency.

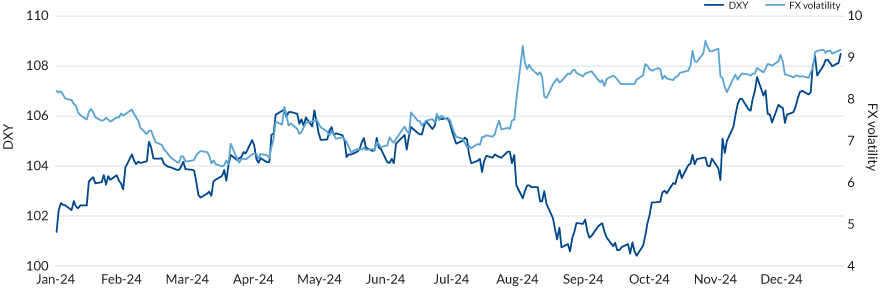

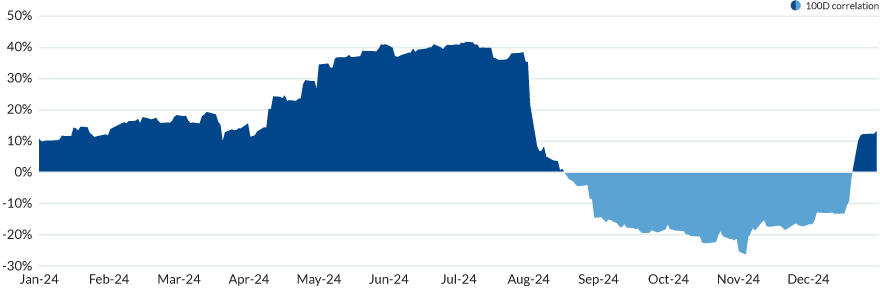

While the US dollar is considered a safe-haven currency, its complexities can periodically steer dollar movements away from risk-on / risk-off market influences. Although uncertainty and volatility continued to play a large role in the dollar movements, their influence waned during the latter part of the past year. For a large portion of 2024, dollar movements were positively correlated with global FX volatility, as measured by the JP Morgan FX Volatility index (Figure 6).

However, the correlation turned negative towards the latter part of the summer months, only to return to positive over the last few weeks of the year (Figure 7).

With Trump entering the White House, financial markets will be influenced by both fiscal and monetary policies in 2025, with FX markets and the US dollar reacting to policy repercussions. We will see if Trump's tariff threats are fully realized or if were they merely a negotiating ploy. The Republican clean sweep implies that policy changes could meet less resistance.

The Fed tilted more hawkish in December, with the dot plot projections lowering to just two rate cuts in 2025. While better relative growth prospects in the US (along with stubborn inflation) support the hawkish tilt, how employment and the economy fare going forward will influence the Fed's path this year, with Trump's policies as a major influence.

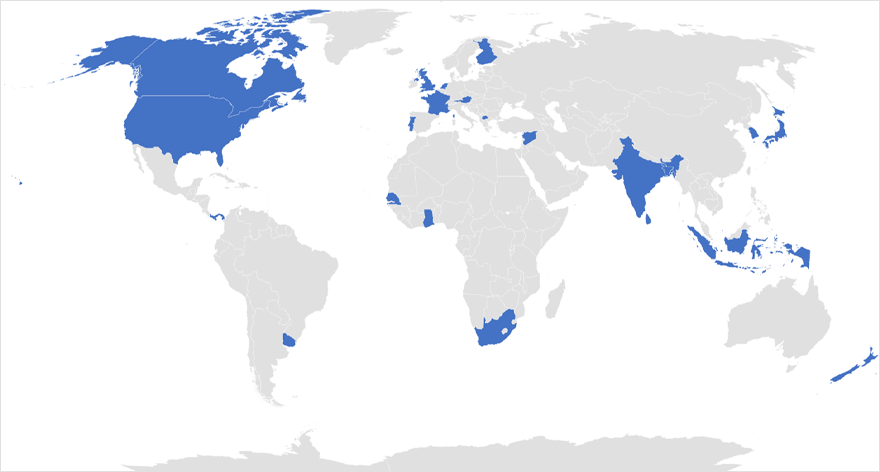

If 2024 acts as a blueprint for 2025, expect more political instability world-wide as incumbents are on watch. Incumbent leadership lost their governing foothold across multiple countries in multiple continents in 2024 (Figure 8), with the trend continuing in 2025 with Trudeau's resignation in Canada and expected change to reach Germany later this year.

With Trump now in office, investors will continue to face uncertainty and market dislocations in the coming year. We recommend that institutions have a currency hedging policy firmly in place ahead of time to responsibly manage currency risk in their international portfolios.

From all of us at Mesirow Currency Management, may the coming year bring happiness and good health.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.