Investors with currency hedging programs are often confronted with positive or negative cash flows when currency forwards are rolled from one settlement date to the next.

For most institutional investors who are typically near fully invested and hold minimal cash, positive or negative cash flows, the result of a realized gain or loss, can pose a challenge. The growing allocation to private assets, which lack the liquidity of traditional stocks and bonds, exacerbates the issue. As a result, large cash flows – especially outflows – can create significant stress for these investors, impacting their overall liquidity management.

In this brief article, we detail different approaches that can help investors manage the liquidity challenges associated with their currency programs more effectively. We will explore four key strategies that investors can utilize to optimize their liquidity management:

Staggering, or laddering, currency forwards is a strategy where an investor enters into forward contracts with multiple settlement dates, rather than relying on a single settlement date. Historically, many investors used one settlement date, which resulted in large, concentrated cash flows. The primary objective of staggering forwards is to smooth out these cash flows over time, reducing liquidity pressure.

For instance, if an investor has a $300 million portfolio that needs to be hedged, they can stagger the notional exposures evenly over three, six, or even 12 months. As the near-term forward approaches its settlement date, it can be rolled forward by another three, six, or 12 months. Generally, bank counterparties require collateral for currency forwards with tenors exceeding 12 months. Therefore, for investors looking to avoid collateralization, it is generally preferable to use forward contracts with tenors shorter than 12 months.

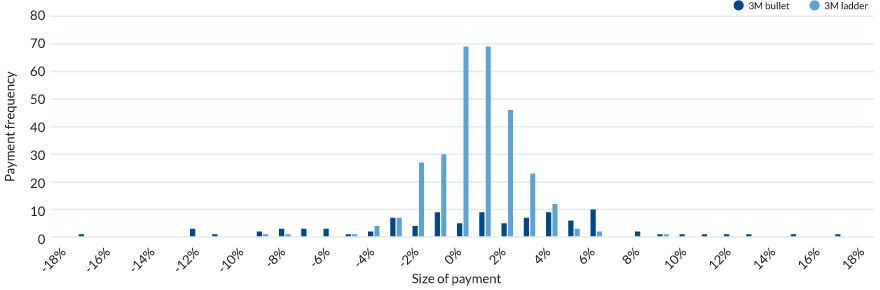

In Figure 1, we compare the payment frequency and size, expressed as percentages, for an Australian investor hedging US Dollars using two strategies:

The payment sizes are significantly larger with the 3-month bullet forward than with the laddered strategy. However, payment frequency is higher with the laddered approach compared to the 3-month bullet forward.

This chart, with hypothetical data, shows the payment frequency and the size of payments on 3-month forward contracts for a sample AUDUSD portfolio. Payment sizes are larger with 3-month bullet forward contracts. Payment frequency is higher with 3-month laddered contracts.

Managing the roll cycle and rolling contracts early can also help investors better manage their cash flows. If an investor lacks immediate liquidity and needs time to raise cash to cover potential losses, they can opt for longer-term contracts, such as six or twelve months, but choose to roll them early.

Instead of waiting until the currency forward approaches its settlement date, the investor can roll the contract ahead of time to crystallize any profit or loss. This can be done at any point before settlement. In many cases, investors choose to roll their contracts one to three months early, depending on their liquidity needs and cash flow requirements.

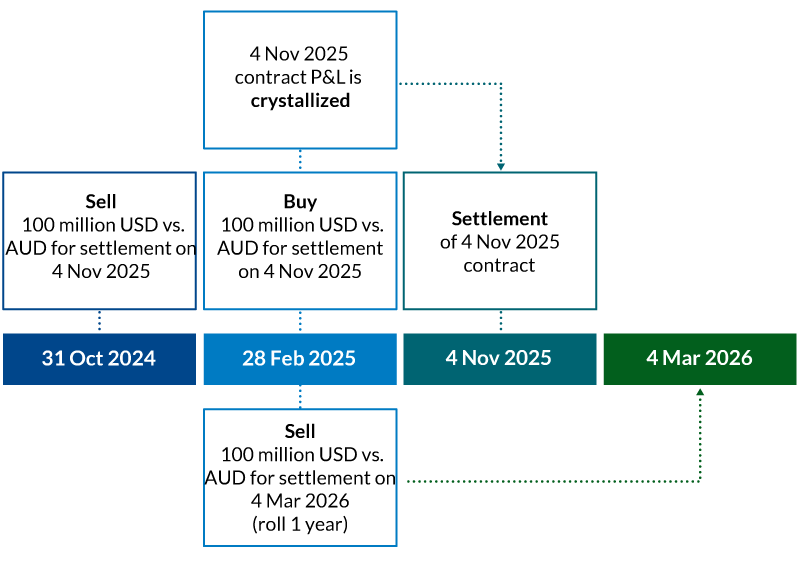

Figure 2 shows a hypothetical roll contract timeline. On 31 October 2024, an investor can sell 100 million USD/AUD for setllement on 4 November 2025. On 28 February 2025, an investor can buy 100 million USD/AUD for settlement on 4 November 2025, sell 100 million USD/AUD for settlement on 4 March 2026 (rolling the contract one year), and the 4 November 2025 profit and loss is crystallized. On 4 November 2025 settlement occurs.

The Historical Rate Rollover (HRR) approach involves rolling an existing currency forward while maintaining the original contract rate, rather than using the current market rate. This strategy helps delay the realization of gains or losses, offering more flexibility and improving cash flow management.

There are, however, some important considerations with HRRs. Not all bank counterparties offer this option, and there is typically an additional cost, as it is akin to a counterparty extending credit by allowing the delay of a loss. Investors should be cautious of this approach. Deferred losses can accumulate significantly if market conditions move unfavorably.

For investors looking to hedge highly illiquid assets with long-dated forwards (greater than 12 months), where collateral may be required by the bank counterparty, a high threshold Credit Support Annex (CSA) can offer a potential solution. The CSA defines the terms of collateral exchange between the investor and the bank, and in this case, the threshold for collateral posting would be set relatively high.

By negotiating high thresholds with multiple bank counterparties and diversifying exposure, an investor may avoid the need to post collateral if the profit or loss stays within the negotiated limits. This approach can provide added flexibility to manage the investor's liquidity.

There are several considerations when using a high threshold CSA. First, the bank counterparty must approve the investor from a creditworthiness perspective, and typically, only investors with strong credit profiles are eligible for this solution. Additionally, a high threshold CSA increases counterparty risk, particularly if the investor's position is profitable, as the bank will not be required to post collateral. Lastly, there is an additional cost, as the bank is effectively providing a line of credit. This charge is generally agreed upon upfront and embedded in the price of the trade.

As investors seek more efficient ways to manage their liquidity and mitigate the stress of funding losses on their currency overlay, one of the approaches described above may prove useful. While this list of liquidity management strategies is not exhaustive, these are among the most commonly used methods. Other potential solutions include options or structured products. However, as with any financial instrument or strategy, it is critical to carefully evaluate both the advantages, disadvantages and associated risks before implementation.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.