The Committee for a Responsible Federal Budget, a nonpartisan group committed to educating the public about US fiscal matters, sent an October 3rd public letter to the presidential candidates urging them to prioritize the burgeoning national debt. The prospective presidents are certain to ignore the plea.

Instead, the candidates are handing out fiscal benefits to voters like homeowners passing out Halloween candy. It would reflect the nation’s situation if homeowners were burdened by crushing home mortgage debt and then took out second mortgages to fund a well-promoted, unbelievably extravagant trick-or-treat give away. That’s because the US debt level is ready to surpass its 1946 historic high with net interest payments of over $1 trillion dollars in 2025. The candidates propose to add to this burden by borrowing between $1.2 trillion and $7.5 trillion over ten years to pay for their campaign promises.

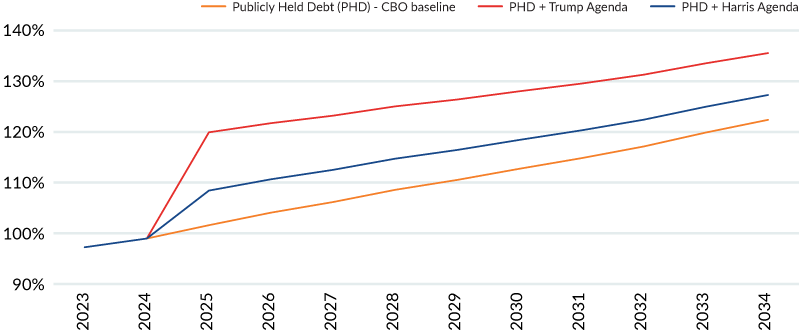

These staggering amounts will increase the Congressional Budget Office’s (a nonpartisan federal agency that provides budget and economic information to Congress) 10-year estimate of publicly held debt by five to 14 percentage points (Figure 1).

The ten-year cost of the presidential hopefuls' pledged generosity is unknown. Campaign promises can be delayed, changed, or unfulfilled depending on the willingness of Congress to fund the promises. That willingness, in turn, can be affected by economic conditions, changing budget demands, and investor enthusiasm to hold more government debt. Still, cost estimates are useful for budget planning and investor assessment of future government finances.

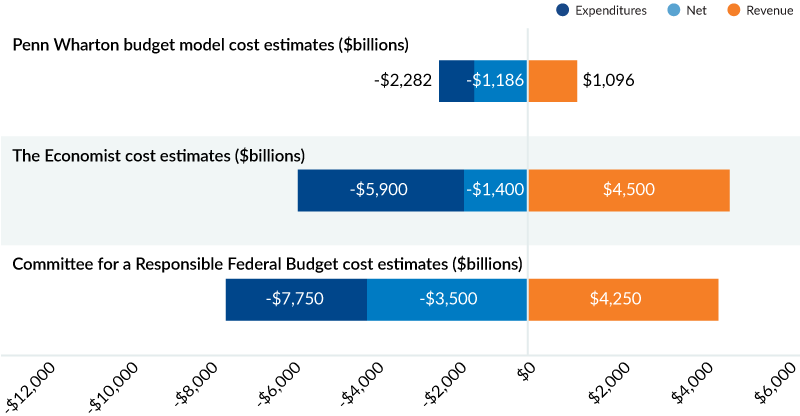

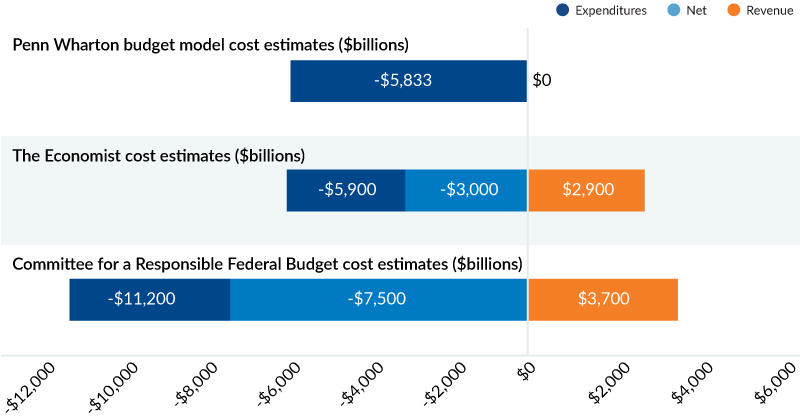

Besides the Committee for a Responsible Federal Budget (CRFB), Penn Wharton Business Model (a non-partisan research group that provides public policy fiscal analyses) and the Economist (a weekly newspaper in magazine format) provided budgetary cost estimates (Figures 2, 3, 4) based on each candidate’s campaign proposals.

Each analysis is based on assumptions that have material effects in determining the net budget impact. For example, CRFB includes tariff revenue in former President Trump’s fiscal analysis, but PWBM ignores that revenue source. PWBM reasons that the tariffs could be offset by retaliatory tariffs and other economic factors. The Economist considers retaliatory tariffs and the dampening effect they would have on US exports; the result is a smaller tariff revenue value compared to CRFB’s estimate.

Vice President Harris offers some of the same fiscal benefits as former President Trump. But unlike the Republican candidate who has all his revenue eggs (tariffs) in one basket, the Vice President has several revenue sources to partially offset the costs. Those sources encompass a higher corporate tax rate, increased capital income taxes and reform of international tax rules, among other funding sources.

Donald Trump continues to add to his proposed tax breaks targeted to specific voter groups, telling the Detroit Economic Club on October 10th that he wants to make car-loan interest payments tax deductible while proposing to offset those costs by charging a 100% tariff on Mexican-made Chinese cars.

Like Halloween, these budget deficit and national debt numbers are frightening. While the presidential candidates shrug off worries about these deficits, debt repayment (CBO estimates net interest will be $1.7 trillion in 2034) will surely haunt the nation.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.