Eleven nations1 have issued central bank digital currencies, a digital form of a government-issued currency that is legal tender but isn't backed by gold or silver (like US dollars). Another 18 countries are piloting CBDCs while dozens of nations are in research or development stages. The United States hasn't decided to issue a central bank digital currency, giving other nations a head start. How will the US's indecision and delay affect the dollar's status as the world's major reserve currency?

That USD reserve currency position is important because it results in lower transaction and borrowing costs for US citizens, businesses, and government; it widens the pool of investors for US investments; and it allows the US to influence global monetary standards. To some, not issuing a CBDC or being a market laggard will give other currencies the opportunity to catch up to or surpass the US dollar's reserve currency position. Others dismiss these concerns; they see little or no connection between central bank digital currencies and reserve currency leadership. Who's right?

Those in the hurry-up-and-issue-a-CBDC camp fear an early launch of China's and other nations' currencies. China's digital currency will provide that nation with more influence with the Mideast, Africa, Southeast Asia, Russia, and other countries. If unchallenged, a Chinese CBDC will become an accepted global currency that will reduce US power in important regions and weaken the effectiveness of economic sanctions that the US relies so often on to achieve foreign policy aims.

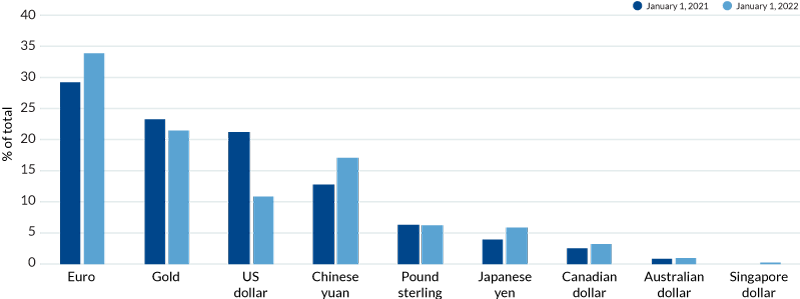

In response to the invasion of Ukraine, the US levied punishing economic sanctions on Russia. The US capped the price of Russian crude oil; blocked Russian banks from using SWIFT, the US-managed global payment system; and froze Russian currency reserves. Russia's response was to increase sales of oil to China and India. Payment for transactions with China were in Russian rubles and Chinese yuan, a step in the direction of making the Chinese currency globally accepted. Even before the war, 17 percent of Russia's foreign currency reserves were denominated in yuan; and among countries, Russia held nearly a third of the Chinese currency.

This group also sees evidence of diminishing effectiveness of US sanctions. A key part of those sanctions is the denial of access to the SWIFT payment system. Alternative payment systems exist, including ones developed by Russia and China. And it's not just US adversaries who are seeking ways to do business outside a dollar-centric world. Ten countries from the European Union2 have joined the Instrument in Support of Trade Exchanges, developed to support legitimate trade with Iran in a 'closed loop' financial system (read: outside of the US payment system).

The combination of a widely accepted central bank digital currency and the overuse of financial sanctions could drive allies and enemies alike away from US-managed financial systems into ones that don't involve the dollar, diminishing the need for US dollar reserves.

Another group sees little threat from CBDCs to the US dollar as the major reserve currency. They note that the change from one dominant currency to another takes decades, pointing to the dollar's slow overtaking of the British pound last century as an example. Those in this camp see digital currencies as no different than currencies in their modern form – government issued without backing by gold or silver. If the dollar hasn't been surpassed by these forms of currencies by now, why would a CBDC that's simply a liability of the issuing nation's central bank be any different?

There are significant reasons why the US dollar is used so often in commerce and finance, reasons that are unlikely to change whether currencies are in central bank digital form or not. The dollar's wide use results in low-cost transactions, even in foreign exchange markets. For transactions involving less traded currencies, both currencies are traded against the dollar instead of directly with each other.

The depth and breadth of US markets and the resulting liquidity are chief reasons foreign nations deal in US dollars. That investment situation is supported by a long-running political and economic stability enhanced with a strong commitment to the rule of law. Those involved in global transactions are unable to find national or regional markets that are superior to US markets; no CBDC – whether foreign or US issued – will change that.

A major benefit of CBDCs is supposedly technological improvements that will settle transactions faster and with more transparency. Those in the CBDCs-are-no-threat group acknowledge that cross-border payments systems need improvement but insist that upgrades are nearing. But even if CBDC transactions are better technologically than the existing settlement process, those improvements will not be significant enough to switch from the dollar. CBDCs are not likely to alter the US dollar's function as a unit of account and store of value.

People could view CBDCs as a solution in search of a problem. Besides potential technological improvements, it is uncertain how CBDCs will enhance international commerce or finance. Central bank digital currencies are in use, however, and more versions are coming. It's involvement – and leadership – that are therefore so important at this early stage. Nations are moving forward with issuing digital currencies, decisions are being made, and systems built. The United States should work with other nations and businesses to develop standards for digital currency privacy protection, communications between systems, compliance protocols, and governance standards. Given the private cryptocurrency implosion, the US could take the lead on regulation, heading off problems with CBDCs that private cryptocurrencies experienced.

And because the capability to apply economic pressure is important to the United States, developing a digital currency and payment system in partnership with allies could be a key factor in foreign policy decisions and actions.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.