In foreign exchange, the most dangerous risks are often found not in the data, but in the assumptions we bring to it. Most of us find FX intuitive on a small scale; we can do the mental math to calculate the dollar cost of a dinner abroad. But as we move toward global trade and macro-policy, that certainty fades. To cope, we reach for simple narratives: a strong dollar is a badge of honor; a weak dollar is a tool for trade dominance. These mental shortcuts are intuitive, often repeated, and – increasingly – wrong.

When these "currency illusions" are adopted by those in decision-making positions, they shift from harmless misunderstandings to dangerous foundations for policy and investment.

These beliefs survive because they feel like "common sense," reinforced by historical anchoring and oversimplified teaching. For decades, the "Japanese Miracle" was attributed to an undervalued yen that weaponized exports. When the 1985 Plaza Accord forced the yen higher, it was blamed for Japan’s "Lost Decades," cementing the myth that a strong currency is a growth killer.

Similarly, academic concepts like Purchasing Power Parity (PPP) – popularized by the Economist's Big Mac Index – suggest currencies should adjust until "stuff" costs the same everywhere.

It’s a clean story that ignores two structural realities. First, PPP excludes non-exportable services; a haircut in Pakistan will always be cheaper than one in Switzerland. Second, global investment flows now dwarf trade flows. The FX turnover in just three business days exceeds total global trade for an entire year. In modern markets, capital flows and interest rate differentials move the needle far more than the price of a burger.

The following illusions appear repeatedly in policy debates and market commentary, simple stories that mask messy truths.

The Myth: The terms "strong" and "weak" are linguistically loaded. We naturally associate a "strong" dollar with American exceptionalism and a "weak" dollar with instability.

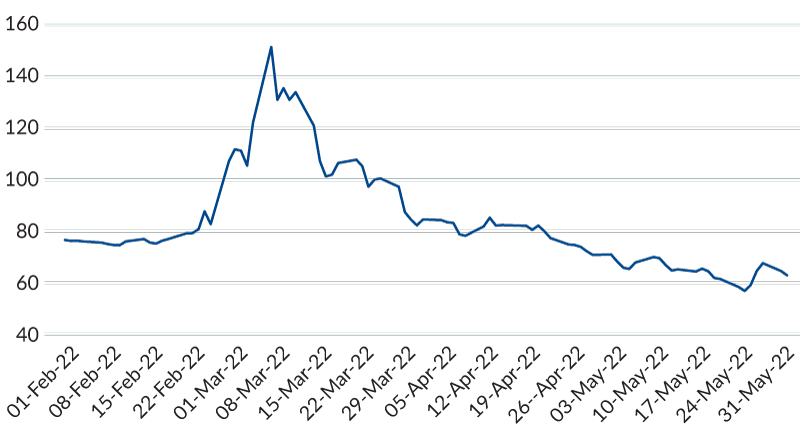

The Reality: Currency strength is a measure of relative demand, not absolute economic health. A currency often climbs not because a country is thriving, but because it is the "cleanest shirt in the dirty laundry" – a safe haven during geopolitical shocks like the U.S. dollar during the Ukraine invasion in 2022.

The extreme "safe-haven" spike is evident as the pair climbed from ~76.00 to over 150 rubles to the dollar in March 2022 following the invasion of Ukraine.

Furthermore, a strong currency is a double-edged sword: while it curbs inflation by making imports cheaper, it acts as a "stealth tightening" of financial conditions. It can choke off exports and erode the earnings of multinationals when their foreign profits are converted into dollars.

In short, a strong currency is often a symptom of high interest rates or global fear, rather than a trophy for economic growth.

The Myth: A weaker currency is often touted as a shortcut to economic growth. The logic is that a lower exchange rate makes domestic goods "cheaper" for foreign buyers, leading to an export boom.

The Reality: In a globalized economy, devaluation is rarely a free lunch. Modern products rely on complex, international supply chains; when a currency drops, the cost of imported components and energy spikes, eating into the price advantage – a reality Japan faced during the "Abenomics" era. Despite a roughly 40% depreciation in the yen against the dollar, Japan’s trade balance failed to improve because firms had already moved production overseas; simultaneously, the cost of imported fossil fuels spiked.

Beyond trade, devaluation often triggers "cost-push" inflation. For firms, a "double squeeze" occurs: they face ballooning costs for materials while interest rates rise to slow inflation caused by the declining dollar.

Ultimately, a devalued currency doesn't create wealth; it redistributes it while inviting systemic risk.

The Myth: Many view the foreign exchange market as a giant poker game where for every dollar gained, someone else must lose a dollar. This logic suggests that currency fluctuations are merely a redistribution of existing wealth.

The Reality: While the transaction itself is an exchange, the economic effects are positive-sum. Currency movements are the "relief valves" of the global economy. When a currency devalues, it is often a necessary adjustment that makes a country’s exports competitive, boosting their production and employment. Conversely, a stronger currency increases the purchasing power of its citizens. By facilitating trade and correcting global imbalances, FX markets help grow the total "global pie" rather than just slicing it differently. Without these shifts, economic pressures would build up until they caused a systemic collapse.

The enduring power of currency illusions lies in the desire to see the exchange rate as a scoreboard – a simple "win" or "loss" for a national economy. But a "strong" currency can be a stealth tightening of financial conditions, and a "weak" one can be an inflationary trap rather than an export engine.

To navigate modern markets, currency movements are better viewed as economic stabilizers rather than competitive trophies. In a globalized system, the exchange rate is the primary mechanism for absorbing shocks and correcting imbalances between nations. Stripping away the linguistic baggage of "strong" and "weak” makes it easier to see there is no "correct" value for a currency – only a price that reflects the messy, constant flow of global capital and trade.

For investors and policymakers, the goal shouldn't be to root for a specific direction, but to understand the trade-offs that every move inevitably demands.

Currency strength is a measure of relative demand, not absolute economic health.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.