Economic fundamentals — growth, inflation and interest rates — once dominated foreign exchange pricing. Today, geopolitical events such as energy disruption, supply-chain realignment and financial sanctions often exert greater influence. Fundamentals still matter, but geopolitics increasingly determine currency direction.

For much of the postwar period, geopolitical shocks influenced exchange rates briefly before fading. Macroeconomic forces—interest rates, inflation, and trade balances—ultimately reasserted themselves, reinforcing the view that geopolitics produced volatility, not valuation.

Today, geopolitical forces increasingly compete with — and at times overwhelm — those macro drivers. During crises, investors rush into safe‑haven currencies, producing sharp rallies that may later fade as tensions ease and fundamentals reassert themselves. But capital flows are now so large and mobile that demand for yield or safety can drive currencies in the opposite direction of what interest rates, inflation, or growth would normally suggest.

Economic fundamentals haven’t disappeared, but they no longer act in isolation. In today’s FX market, fundamentals interact with trade policy, central‑bank signaling, sanctions, and fast-moving speculative capital. The result is a market where shocks do not merely trigger short-term moves, but force investors to price longer‑term risks — supply disruptions and sustained geopolitical tension — into currencies. Geopolitics has shifted from episodic headline risk to a persistent force shaping FX outcomes.

In earlier decades, discrete geopolitical shocks tended to create sharp but mostly temporary market effects. In an analysis of 70 geopolitical shocks since 1970, Schwab found that geopolitical events often generated short‑term volatility without long‑lasting market impacts, with prolonged negative effects more likely when shocks coincided with recessions.

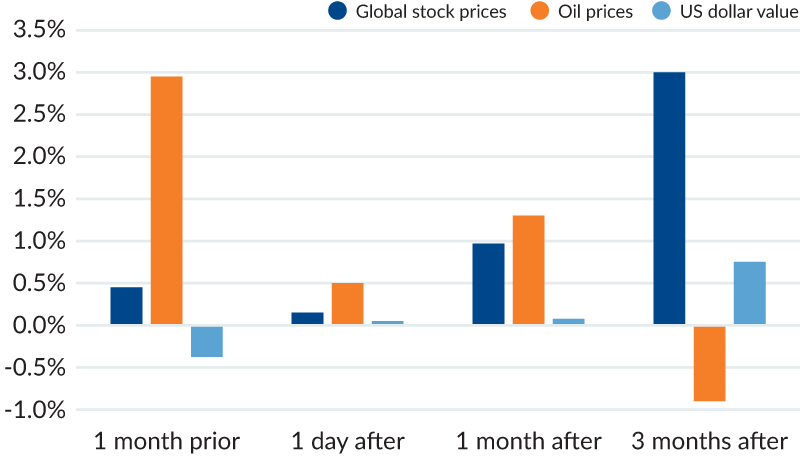

Figure 1 illustrates how market dislocations around geopolitical events were typically front‑loaded and often mean‑reverting over subsequent months. These patterns reinforced the belief that geopolitical shocks were volatility, not valuation, events.

What has changed is not that every shock is permanent, but that markets now operate in an environment of geopolitical “fracturing”—the breakdown of economic and financial integration between nations. Fracturing can produce higher inflation risk, more frequent supply shocks, and longer bouts of volatility.

Trade policy is a key driver of this persistence: tariff regimes are political, reversible, and often contested, keeping uncertainty elevated. Sanctions are more persistent by design because they rewire the plumbing of cross‑border finance. Russia’s experience illustrates the effect: settlement constraints created conversion bottlenecks where liquidity existed, but convertibility did not. “Everyone is sitting on rubles. There’s a ton of liquidity, but nowhere to convert it,” one bank employee said in 2024.

When investors flee chaotic currencies, they reach instinctively for safe havens. But the definition of a safe haven has evolved. Today, demand depends less on reputation than on financial infrastructure, market depth, and institutional credibility.

On those measures, the U.S. dollar still dominates. The market for U.S. Treasuries remains the largest and most liquid pool of securities in the world, and dollar funding underpins global trade, derivatives, and cross‑border banking. In moments of stress, no other currency can absorb capital flows at a comparable scale.

Liquidity, scale, and institutional access now define safe-haven status (Table 1).

Yet safe‑haven status now rests on more than liquidity. Trust matters — and not merely historical trust. Investors increasingly judge countries by the current health of their fiscal position, the predictability of policy, and the perceived stability of institutions. History, in other words, is no longer a sufficient credential.

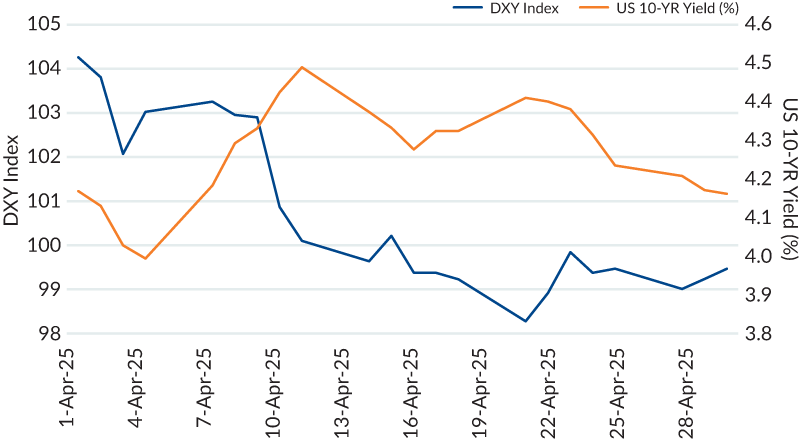

That reassessment has become visible in market behavior. Research from State Street shows that the long‑standing positive relationship between U.S. Treasury yields and the dollar has weakened. One visible episode came in April 2025 when yields on long‑dated Treasuries rose sharply even as the dollar fell — a rare divergence that reflects investor unease. Rather than viewing higher yields as evidence of economic strength, markets interpreted them as compensation for fiscal risk, policy uncertainty, and rising debt.

This does not signal the end of dollar dominance. But it does suggest that the dollar’s safe-haven premium has become more conditional — anchored less in history, more in ongoing credibility.

Macroeconomics moves currencies gradually. Geopolitics reprices them abruptly.

Macroeconomic forces still shape currencies — but they do so gradually. Interest‑rate differentials, inflation trends, and trade balances typically move exchange rates through slow changes. Even surprises, while sometimes sharp, tend to be absorbed over time.

Geopolitics works through a different transmission mechanism. It reprices currencies through sudden shifts in confidence and alignment, often bypassing traditional macro channels altogether.

Confidence and alignment determine how currencies respond to geopolitics — both immediately and over time.

Confidence governs the immediate FX response: liquidity, convertibility, and institutional reliability determine whether capital stays or flees. Alignment shapes longer‑term currency paths by redirecting trade, capital, and reserve flows toward trusted networks.

Central banks reinforce these dynamics. Reserve diversification, swap‑line access, and trade‑settlement choices increasingly reflect geopolitical considerations. As alignment strengthens, currencies benefit from persistent demand; as geopolitical risk rises or alliances fray, they depreciate — often sharply.

In short, confidence determines the shock; alignment determines the path. Together, they explain why geopolitics now moves FX in ways macroeconomics alone cannot.

To many observers, currency markets appear untethered from economic data. Robust growth can coexist with weak currencies; higher interest rates do not reliably attract capital.

Macroeconomic fundamentals still matter, but they are often overridden by geopolitical forces. Capital now moves less in response to marginal yield changes and more in response to perceived political trajectories.

These shifts are rarely incremental. During geopolitical shocks, capital flows can overwhelm liquidity, disrupt funding markets, and force abrupt changes in central‑bank reserve management. Exchange rates can move in ways that appear detached from data releases because markets are pricing future political states, not present economic conditions.

The global order is no longer cohesive. Long‑standing alliances are under strain, trade is increasingly weaponized, and nations are reorganizing finance and supply chains around security as much as efficiency. Currencies — deeply embedded in these structures — cannot escape the turbulence.

Foreign exchange has become a market for probabilities—not forecasts of growth or inflation, but judgments about trust, alignment, and political durability.

The implications are stark. Governments that strengthen institutions, maintain policy credibility, and remain integrated into global networks position themselves on the right side of capital flows. Those that do not face currency depreciation, higher funding costs, and domestic instability.

The choice is conceptually simple, but politically hard. In a world of persistent geopolitical risk, confidence must be earned, renewed, and defended.

Governments that strengthen institutions, maintain policy credibility, and remain integrated into global networks position themselves on the right side of capital flows.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.