The massive EU-Australia Free Trade Agreement is set to make a major mark on global trade while intensifying an existing currency divide. By linking the European Union closely to Australian critical minerals and Indo-Pacific growth, the pact strengthens the euro's role as an engine for commerce and expansion. Because Switzerland belongs to a separate trade group, it sits outside the pact. This leaves the Swiss franc increasingly defined by its traditional role as a refuge for capital during periods of uncertainty.

The agreement deepens Europe's two-currency reality and illustrates how modern trade agreements increasingly shape currency behavior.

In today’s world of supply-chain vulnerabilities, economic fragility and shifting strategic resilience, trade pacts can be a component of much broader relationships. The EU-Australia FTA illustrates this trend: the two parties announced trade negotiation success alongside a broader security and defense partnership.

The agreements were shaped by the EU’s experience with Russian energy and Australia’s over-reliance on China as a primary export market. The Russian energy embargo beginning in 2022 highlighted dangers of supply-chain exposure to a single provider while Australia chafed at trade coercion with the Asian superpower.

Additionally, the EU wanted to be better integrated with the Indo-Pacific region that Brussels believed would be important in world economic growth, strategic competition and supply-chain activity. Australia was an attractive Indo-Pacific partner because it shares similar views with Europe on open trade, democratic institutions and rules based international order.

While omitted from official press releases, the pact also serves as a mutual buffer against rising U.S. protectionism and the intensifying U.S.- China rivalry.

The economic pact and the overarching defense arrangements are mutually reinforcing. While the trade deal secures deep economic integration, the parallel strategic agreements fortify political, technological, and supply-chain resilience across both hemispheres.

Although the agreement delivers benefits to both sides across trade, investment, and security, the underlying strategic priorities are not identical. Australia is primarily seeking diversification and resilience, while Europe is focused on supply-chain security and a stronger Indo-Pacific presence.

Australia wants diversification. Europe wants minerals and Indo-Pacific influence.

Investors have always navigated a fragmented European currency landscape. This division simplified in 1999 when eleven nations adopted the euro. While ten more nations subsequently joined the Eurozone, Switzerland maintained its franc. Although the EU and Switzerland remain deeply intertwined economically, their currencies serve fundamentally different purposes. Investors associate the euro with trade, growth, and structural integration, while the Swiss franc operates as a premier global safe haven during market duress.

The EU-Australia trade agreement does not alter this structural relationship. Instead, it incrementally anchors the euro to global trade flows, critical minerals, and Indo-Pacific expansion. Modern trade pacts now look past simple tariff elimination; they establish supply chains, technological alliances, and security framework parameters. Consequently, they exert a heavy influence on the geopolitical forces driving long-term currency demand. Currencies, in essence, increasingly reflect geopolitical alliances.

The euro becomes linked to:

while the franc remains outside of those structures, emphasizing its role as a:

Exclusion from the EU-Australia FTA preserves the core strength of the Swiss franc. Its safe-haven status is anchored to centuries of political neutrality and strict fiscal discipline rather than trade networks.

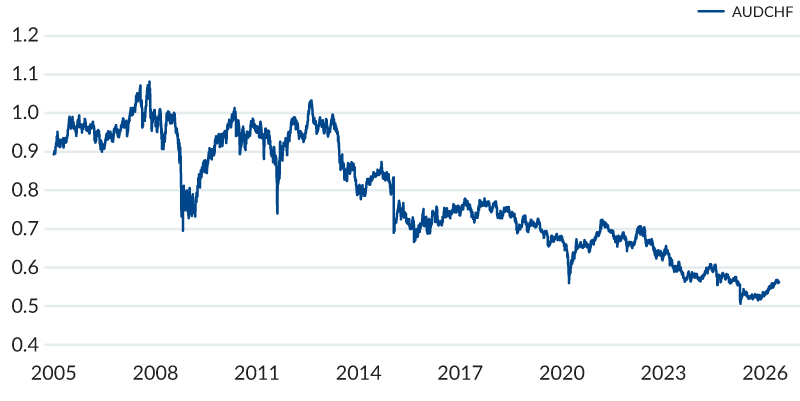

For more than a decade, the Australian dollar has trended down against the franc.

For some investors, the Swiss franc may serve as a potential hedge against periods of geopolitical stress or global trade disruptions. This dynamic can yield dual benefits: local asset returns combined with positive currency translation gains.

While the trend in the AUD/CHF exchange rate has been historically consistent, investors need to proceed cautiously because the two currencies are ideal candidates of a tempting carry trade. This strategy involves selling a low-interest rate currency and buying a high-interest rate one. The investor collects the net interest-rate spread.

The Swiss National Bank (SNB) maintains its benchmark policy rate at 0% amid subdued inflation pressures and the persistent strength of the Swiss franc. The Reserve Bank of Australia (RBA) maintains its cash rate at 4.35% after three rate hikes in 2026 aimed at containing persistent inflation pressures.

The wide difference between Swiss and Australian rates makes a carry trade alluring. But wariness is warranted: Because the SNB actively intervenes in foreign exchange markets, the franc does not behave like a pure free-floating currency. Trading AUD/CHF is therefore not just a bet on Australian commodities or Swiss financial institutions—it is also a bet on how the SNB responds to currency movements. The worry is real: The SNB triggered a famous euro – Swiss franc reversal in 2015 that wiped out years of carry trade gains.

The macro shifts illustrated by the EU–Australia pact are mirrored in other sweeping, structural trade agreements globally.

The EU–Australia agreement underscores a fundamental shift in global finance. Modern trade agreements are no longer merely instruments for lowering tariffs. They increasingly bind countries through supply chains, critical minerals, technology partnerships and security cooperation. As these networks deepen, currencies may reflect not only economic fundamentals but also geopolitical alignment. For investors, understanding trade blocs increasingly means understanding currency blocs.

The agreement deepens Europe's two-currency reality and illustrates how modern trade agreements increasingly shape currency behavior.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.