In a 2026 speech at the World Economic Forum, Canadian Prime Minister Mark Carney argued that the global order has been shattered. Strong nations increasingly act solely in their own interests, while weaker countries “go along to get along.” Carney urged middle powers—nations that can influence but not dominate global outcomes—to strengthen cooperation in energy, food production and defense without abandoning values such as human rights and sustainability.

Carney was effectively promoting reglobalization: a trade, financial, and security model in which nations cluster around regional interests, political similarities, and shared values. Reglobalization would almost certainly be less efficient and more costly than the globalization framework that has prevailed since World War II. But for many countries, working with like-minded partners may be more appealing than relying on a system dominated by a superpower with the “market size, the military capacity, and the leverage to dictate terms.”

But breaking away from a U.S.-centric world, the unnamed superpower in Carney’s comments, will not be easy.

Today’s debate has deep roots in the post–World War II Bretton Woods system, under which the United States agreed to convert dollars into gold at $35 per ounce. Other nations maintained fixed exchange rates against the dollar rather than directly linking their currencies to gold.

When Bretton Woods collapsed in the early 1970s, the world moved from a gold-anchored system to floating exchange rates where currencies derive their value from market supply and demand.

At the time, many economists predicted that the dollar’s dominance would fade—much as Britain’s pound sterling had gradually lost its preeminence in the early 20th century. Analysts watched central bank reserve holdings for signs that another currency would displace the dollar.

They are still watching.

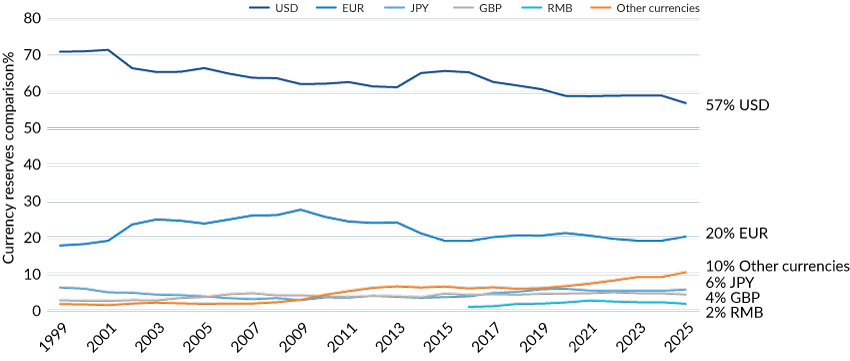

Although the dollar’s share of global reserves has gradually declined over the past 25 years (FIGURE 1), no currency is close to replacing it.

Undeterred, critics now argue that the system is evolving toward a tri-currency world of dollar, euro, and renminbi blocs. Measured by gross domestic product, it is tempting to argue that three blocs already exist (Table 1).

But GDP size alone does not create a reserve currency

The euro continues to face structural challenges, including fragmented fiscal governance and periodic debt crises. The renminbi remains constrained by capital controls, limited convertibility, and uncertainty regarding state intervention in financial markets.

Meanwhile, the dollar retains commanding advantages across multiple dimensions:

The dollar’s reign is not over.

What frustrates U.S. rivals is not merely the dollar’s ubiquity. It is that the United States sits at the center of the global financial architecture.

As Carney put it: “Great powers have begun using economic integration as weapons—tariffs as leverage, financial infrastructure as coercion, supply chains as vulnerabilities to be exploited.”

Because global trade and finance are deeply dollar-based, the United States exercises significant influence over who can transact in dollars, which banks can access dollar clearing, and which firms or individuals are excluded from the system.

One important mechanism is the U.S. government’s influence over dollar clearing and its ability to impose financial sanctions. While SWIFT—the global financial messaging network—is headquartered in Belgium and not owned by the United States, U.S. sanctions policy can effectively pressure institutions to disconnect targeted banks. Exclusion from SWIFT or dollar clearing significantly raises the cost and uncertainty of cross-border transactions, pushing sanctioned countries toward the margins of global finance.

Tariffs are more visible. Used as instruments of economic statecraft, tariffs can coerce policy change or reward favored trading partners. Whether one calls this leverage or bullying depends on perspective.

Proponents of a multipolar currency system argue that three blocs are emerging.

This bloc centers on the United States and includes advanced economies and long-standing allies such as Canada, Mexico, Japan, Australia, South Korea, and much of Europe. These nations rely heavily on the dollar, cooperate on supply chain resilience and technology development, and maintain deep defense relationships with Washington.

The dollar bloc benefits from deep capital markets, strong rule of law, technological leadership, and flexible crisis response.

The euro bloc is more regulatory and consensus driven. Its members share a common currency across much of Europe and are increasingly focused on “strategic autonomy” in energy, semiconductors, and defense.

But governance remains complex. The need for multi-country consensus slows decision-making. Although aligned with the United States on many security issues, European policymakers often seek to hedge against overdependence on U.S. leadership.

China anchors the third bloc. It maintains strong trade relationships across Asia, Africa, and Latin America and dominates global manufacturing in areas such as electric vehicles and battery technology.

Yet the renminbi faces structural obstacles: capital controls, relatively shallow financial markets, and persistent concerns about legal transparency and state intervention. China remains dependent on foreign intellectual property and advanced semiconductor technology, even as it works aggressively to close that gap.

Its export-driven model also creates tensions, as domestic industries in trading partners compete with Chinese manufacturing scale.

Table 2 summarizes the blocs.

Many countries have experimented with workarounds to reduce exposure to U.S. financial power: settling trade in local currencies, developing alternative payment systems, using intermediaries or even resorting to barter arrangements. These methods can function—but often at higher cost and lower efficiency.

Trade agreements are another response. After years of negotiation, Europe recently advanced trade agreements with Mercosur nations and India. Such agreements aim to diversify economic relationships and reduce reliance on any single partner. But Europe’s regulatory structure and judicial review processes mean implementation is often slow.

BRICS—Brazil, Russia, India, China, and South Africa plus five other nations—has positioned itself as a counterweight to Western dominance. Its objectives include expanding geopolitical influence, reducing dollar dependence, and promoting a multipolar financial order.

Since its first summit in 2009, BRICS has proposed ambitious initiatives: a common currency, alternative payment systems, and digital settlement platforms. Progress has been uneven. The New Development Bank operates, but on a modest scale relative to the World Bank. BRICS Pay remains in pilot phases.

Internal competition complicates matters. China, India, Russia, and Brazil each have national payment systems and global ambitions. Trust is limited. No member wishes to subordinate its financial infrastructure to another—particularly China.

In the meantime, BRICS members increasingly settle trade in national currencies. China’s renminbi accounts for a growing share of intra-BRICS trade settlement, reflecting China’s economic weight and strong nation behavior.

Despite mounting efforts to build alternatives, the global system remains overwhelmingly dollar centered.

Can it endure indefinitely? History suggests that no international monetary order lasts forever. Persistent challengers—especially large economies like China—will continue pushing for alternatives. Middle powers, frustrated by sanctions or tariff pressure, will continue seeking diversification.

Yet for now, the dollar’s network effects, liquidity, legal infrastructure, and institutional depth remain unmatched. And if instability encourages middle powers to strengthen their own supply chains, militaries, and industrial capacity, that may not signal the end of the system but rather its adaptation.

The question is not whether the world order is changing. It is whether change will be evolutionary—or disruptive.

Is the global monetary system fragmenting into three currency blocs?

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.