Does more data mean better models? Maybe not for neural network systematic FX trading strategies. In this paper, we explain a qualitative approach to estimating the optimal look-back window size to create training sets for deep neural network-based FX strategies.

Machine learning-based systematic FX trading algorithms utilise training sets to learn optimal model parameters. These training sets are usually constructed from various time series, sometimes with different granularities, and the main training set is usually split into several subsets to perform training, validation, model selection, and (simulated) out-of-sample evaluation.

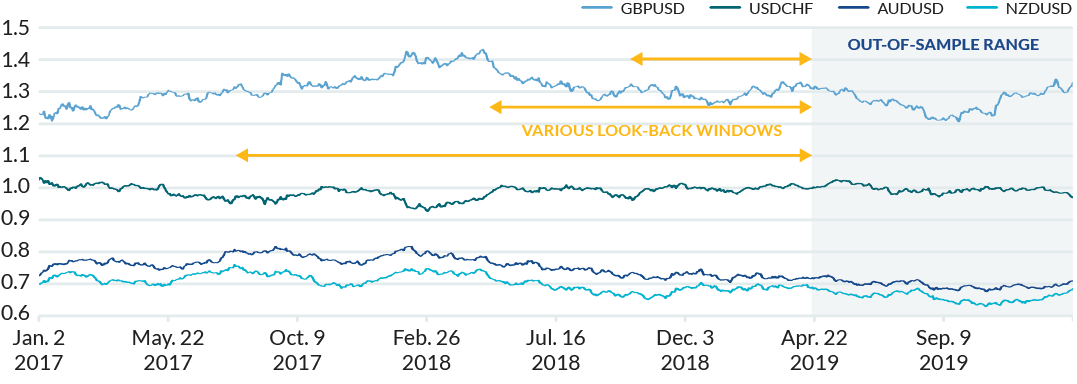

A common approach to extracting training samples from raw sequential data is to allocate a (temporal) look-back window (LBW) length. To capture the latest market trends, these LBWs are usually selected to be close in time to the out-of-sample period. Different LBW sizes generate different training sets with their own specific statistical features. In Figure 1 we show daily spot FX rates for four (example) currency pairs. While the gray area shows the out-of-sample (test) range, various LBWs (shown as yellow arrows) can be used to construct different training sets.

The captured samples within the selected LBW range are then pre-processed and prepared for the next steps. Stationarity analysis may be necessary if the statistics of the signal change over time. Another step could be normalisation: the input signal to a machine learning pipeline is usually normalised, which can be an extremely important part of its learning performance.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.