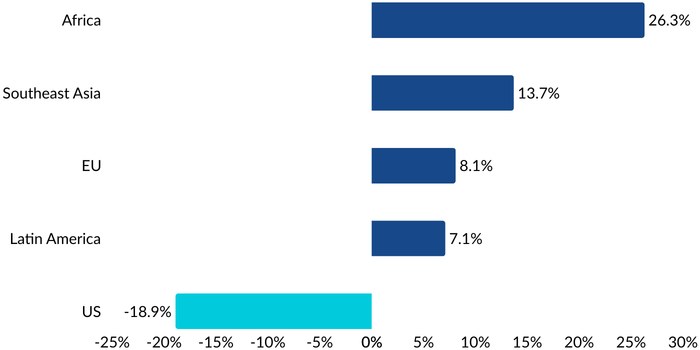

“The tariffs are making them [US farmers] rich,” President Trump declared in December 2025. He was referring to a $12 billion aid package designed to offset, at least in part, lost agricultural sales to China following Beijing’s retaliation against US tariffs. China, refusing to yield to tariff pressure, has seen its exports to the United States fall by roughly 19 percent. Yet sales to other regions more than compensated for the decline in US demand.

Figure 1 illustrates how China redirected exports in response to tariffs - an example of how trade flows adjust when barriers rise. Less visible, but no less important, is the chain reaction tariffs set in motion (Figure 2) across inflation, monetary policy, and foreign-exchange markets.

Tariffs raise prices for at least one party in the import chain — and often for several. The burden can fall on foreign producers that accept lower prices, US importers that absorb higher costs through thinner margins, or consumers who ultimately pay more at the checkout counter, reducing real after-tax incomes.

In practice, foreign producers rarely shoulder much of the cost. During the 2018–2019 tariff episode, roughly 80 percent of tariffs were passed through to US import prices. In 2025, estimates suggest pass-through rose to about 94 percent. That outcome reflects the mechanics of tariff collection: by law, US importers pay tariffs when goods enter the country. Whether those costs are passed along to wholesalers, retailers, and consumers depends on market structure, pricing power, demand elasticity, and competitive conditions (Table 1).

Empirical evidence confirms the inflationary effect. The Budget Lab at Yale University found that core goods prices in the Personal Consumption Expenditures index rose 1.5 percent through June 2025, compared with just 0.3 percent in the same period a year earlier. Durable goods prices increased 1.7 percent, reversing a 0.6 percent decline in early 2024. Imported core goods and durable prices rose even faster, outpacing broader inflation trends.

Other studies estimate that tariffs added between 0.1 and 0.8 percentage points to annual inflation, with substantially larger effects in sectors such as durable goods and electronics (Table 2).

Tariffs rarely stop at the border. The US 2025 tariffs on steel and aluminum, along with duties of 10 to 50 percent on a wide range of other goods, rippled through North America’s tightly integrated supply chains, hitting the automotive and electronics industries particularly hard. Electric vehicle manufacturers felt the impact quickly, as costs jumped for imported batteries and rare earth minerals essential to production.

Those rising costs bred uncertainty. Would tariffs climb further? Should manufacturers scramble to find domestic suppliers, even if that meant abandoning just-in-time logistics? The lack of clear answers complicated planning and pushed some investment decisions to the sidelines.

As companies adjusted, global supply chains shifted. Countries such as Vietnam, Mexico, and India emerged as alternatives to China for low-cost, labor-intensive production, in part because they faced lower effective tariff burdens. Some firms responded by nearshoring—moving production closer to final markets in North America to reduce risk while preserving cost advantages. But the broader picture was less orderly: trade-weighted tariffs ranging from 2 to 24 percent fragmented supply chains and increased logistical complexity.

Tariffs complicate the task of central banks by pulling monetary policy in opposing directions. By raising prices, tariffs argue for higher interest rates to contain inflation. At the same time, they can weigh on growth and employment, strengthening the case for lower rates. Faced with these crosscurrents, central banks may hesitate, waiting for clearer evidence of how tariffs are filtering through the economy. That caution can heighten market uncertainty and spill over into asset prices.

US Federal Reserve Chair Jerome Powell made that tension explicit at a December 10 press conference. He pointed to tariffs as the main reason inflation—running at about three percent in September 2025 before declining to 2.7% at the end of the year —remained above the Fed’s 2 percent target. “It’s really tariffs that are causing most of the inflation overshoot,” Powell said. He described the impact as a “one-time shift in the price level” rather than a persistent trend but stressed the Fed’s responsibility to prevent those price increases from becoming entrenched.

Against that backdrop, Powell characterized the Fed’s December decision to cut the federal funds target range by a quarter point, to 3.5 – 3.75 percent, as a balancing act. Inflation risks remained tilted upward because of tariffs, he said, while employment risks had risen as the labor market cooled.

Central banks with a dual mandate – such as the US Federal Reserve, which targets both inflation and employment – have more scope to strike that balance. Institutions focused primarily on price stability, including the European Central Bank and the Bank of England, have tended to place greater weight on inflation risks, even as tariffs weighed on trade and growth.

Table 3 summarizes interest-rate changes at major central banks in 2025 and how US tariffs factored into their policy decisions.

In the short term, foreign-exchange markets proved highly sensitive to tariff headlines and the fear they triggered. Over longer horizons—measured across the calendar year – those shocks tended to fade. Tariffs emerged less as enduring drivers of currency direction and more as episodic stresses, quickly absorbed and overtaken by trends specific to individual currencies.

Standard currency theory would suggest that US tariffs should strengthen the dollar. Higher import prices reduce demand for foreign goods, lessening the need to sell dollars to buy foreign currency. In practice, the market response was more complex.

Against the Japanese yen, a traditional safe-haven currency, the dollar initially weakened before bottoming in April and climbing steadily through the rest of the year. By year-end, the dollar was just about flat against the yen (Wall Street Journal, January 2, 2026). Differences in growth prospects and interest-rate differentials – lower in Japan, higher in the United States even after rate cuts – diminished the yen’s defensive appeal.

The picture was more volatile elsewhere. Against the Swiss franc and the DXY index, which tracks the dollar against a basket of six major currencies, the dollar fell sharply in April as investors rushed to safety. Once the immediate tariff shock passed, markets reassessed. Investors concluded that tariff damage would be uneven and slower to materialize than initially feared. In the second half of the year, both the franc and the DXY traded in choppy ranges as markets waited for clearer answers: would tariffs prove primarily inflationary, growth-limiting, or both?

Safe-haven demand did not disappear, but it became more selective and tactical rather than a one-way bet. The experience of the Chinese yuan underscored that shift. Despite an escalating trade confrontation with the United States, China—the world’s manufacturing hub and second-largest economy – managed a gradual appreciation of the yuan against the dollar of roughly 4.35 percent over the year. That decline was punctuated by sharp volatility around “Liberation Day,” reflecting a moment of heightened confrontation between two economic superpowers. Markets ultimately treated tariffs on China as a risk, but not one likely to trigger a collapse in global trade.

The broader lesson was clear: tariffs mattered in currency markets, but mainly as short-term shocks rather than long-term determinants of exchange-rate direction.

Tariffs in 2025 arrived with shock and awe – and then, for many observers, turned into a shrug. The surprise sparked by the scale and scope of the April tariff announcements gradually gave way to exemptions, workarounds, negotiations, and outright avoidance. By year-end, effective tariff rates were roughly half the levels initially announced. Even so, tariffs left their mark, pushing up inflation, complicating monetary policy and temporarily disrupting currency trends.

Businesses and consumers have continued to produce and spend. Yet against a backdrop of rising geopolitical tensions, elevated equity valuations and persistent concerns about affordability, tariffs remain a wild card. Their effects are diffuse, uneven, and difficult to predict. Some investors have responded by hedging US exposure through foreign-exchange strategies, using forwards or options to guard against downside risk. Others have turned cautious, holding cash while waiting for clearer signals – and better entry points. For households, the adjustment is more practical than strategic. Tariffs mean higher prices, tighter budgets, and more careful timing of major purchases. The takeaway is less about financial engineering than flexibility: saving more where possible, spending deliberately, and recognizing that tariffs are likely to remain part of the economic landscape for some time.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.