Financial planning is a crucial aspect of family life. From managing day-to-day expenses to preparing for major life events, families must navigate a complex landscape of financial decisions. It is easy for the demands of daily life to take precedence — from coordinating schedules for extracurricular activities, to planning birthday parties, or even simply planning a weeknight dinner. This article addresses five key financial planning topics that should be prioritized when trying to accomplish financial goals on top of day-to-day demands.

The first step in financial planning for families starts with having a conversation. Discussing money is not always the easiest and most comfortable topic, but regular discussions can help align priorities, identify potential challenges and foster a sense of shared responsibility.

To kickstart your financial planning discussion, it's essential to gather all pertinent financial information and create a family balance sheet. Items to include are:

Going through this exercise at least once a year and putting pen to paper is incredibly valuable. It allows you to track progress and make sure both partners are on the same page.

In conjunction with creating a balance sheet, families should openly discuss their short-, medium-, and long-term goals. The key to financial planning is prioritizing your goals. We can't achieve all our goals at once but breaking them down into time periods and prioritizing them makes achieving them a lot more tangible.

Estate planning is not just for the "rich." Estate planning involves creating a plan for the distribution of assets and properties after one's passing. It's a critical component of financial planning that ensures the smooth transfer of wealth and minimizes potential conflicts among heirs. Families should consider drafting essential documents such as wills, trusts, and powers of attorney to outline their wishes and protect their loved ones' interests. By proactively addressing estate planning matters, families can provide peace of mind and clarity for the future.

Here are the most important estate planning items for young families to consider:

Insurance plays a vital role in mitigating financial risks and protecting against unexpected events. Families should assess their insurance needs across various areas, including health, life, property and liability. Adequate coverage can safeguard against medical expenses, property damage, legal liabilities, and loss of income due to disability or death. By reviewing insurance policies regularly and adjusting coverage as needed, families can ensure comprehensive protection for themselves and their assets.

Life insurance is an important component for families to consider when evaluating their financial plans. Understanding the types of policies available is key when evaluating what makes sense for a family's needs:

What is life insurance? Insurance on your life! Meaning if you pass away, the insurance company pays your beneficiary (usually the surviving spouse) an agreed upon lump sum.

A 529 plan is a state-sponsored savings vehicle designed specifically to address qualified education expenses. Every 529 plan has one account owner, often a parent or grandparent, and one designated beneficiary.

Importantly, anyone can contribute to a child's 529 plan, so if grandparents want to give gifts to their grandkids, this is a great place to do it!

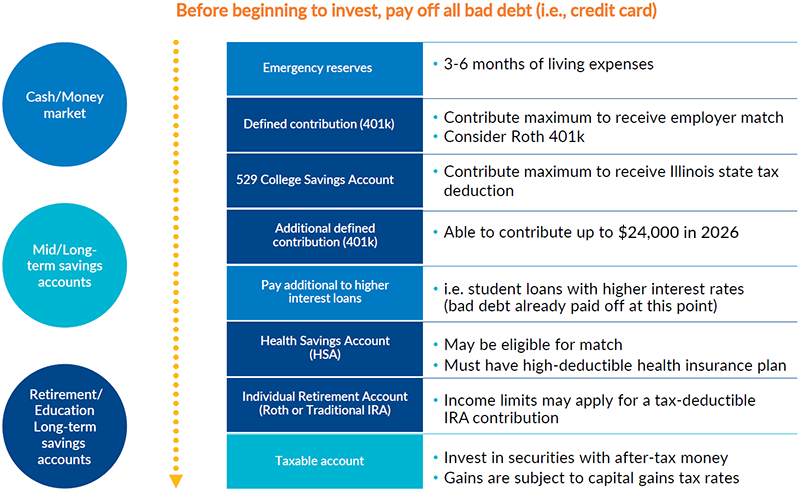

With numerous financial goals competing for attention, prioritizing savings can be challenging. Families should evaluate their objectives and allocate resources based on their importance and urgency. Essential considerations include building an emergency fund to cover unexpected expenses, paying off high-interest debt to reduce financial strain, and investing for long-term growth. By establishing clear priorities and adopting a disciplined approach to saving, families can make meaningful progress towards their financial goals while maintaining financial stability.

This chart below is an example of how/where to start:

Financial planning is never one size fits all. By addressing these key considerations proactively, families can strengthen their financial well-beings, protect their loved ones, and work towards a more secure future. Through collaborative decision-making and a commitment to financial responsibility, families can navigate the complexities of financial planning with confidence and clarity.

Collaborating with a financial advisor enables your family to define its objectives and assess its financial standing to successfully achieve your goals. This partnership not only empowers you to make informed decisions but also grants you the freedom to cherish the most fulfilling aspects of family life without the burden of financial worries.

Mesirow Wealth Management is a division of Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor. Securities offered through Mesirow Financial, Inc., member FINRA, SIPC. Advisory Fees are described in Mesirow Financial Investment Management Inc.’s Part 2A of the Form ADV. Mesirow refers to Mesirow Financial Holdings, Inc. and its divisions, subsidiaries and affiliates. The Mesirow name and logo are registered service marks of Mesirow Financial Holdings, Inc.